Introduction

The Common and Emerging Practices, a new series of resources from the Impact Principles, aims to capture key insights from notable trends in common practices in implementing the Impact Principles by our Signatories and highlight promising emerging practices and key gaps. By sharing these common and emerging best practices in impact management, we seek to elevate impact practice in the market and ensure that capital is mobilized at scale with integrity to drive meaningful impact outcomes.

The resources related to Common and Emerging Practices will be released in phases through website publication of initial drafts for each of the nine principles in series, followed by draft and final consolidated reports with stakeholder engagement.

Principle 4

Assess the expected impact of each investment, based on a systematic approach

For each investment the Manager shall assess, in advance and, where possible, quantify the concrete, positive impact potential deriving from the investment. The assessment should use a suitable results measurement framework that aims to answer these fundamental questions: (1) What is the intended impact? (2) Who experiences the intended impact? (3) How significant is the intended impact? The Manager shall also seek to assess the likelihood of achieving the investment’s expected impact. In assessing the likelihood, the Manager shall identify the significant risk factors that could result in the impact varying from ex-ante expectations. In assessing the impact potential, the Manager shall seek evidence to assess the relative size of the challenge addressed within the targeted geographical context. The Manager shall also consider opportunities to increase the impact of the investment. Where possible and relevant for the Manager’s strategic intent, the Manager may also consider indirect and systemic impacts. Indicators shall, to the extent possible, be aligned with industry standards and follow best practice.

The Components of Principle 4

- Assess and quantify potential positive impact from each investment

- Use a results framework answering the intended impact, who experiences it, how significant it is and the likelihood of achieving it

- Assess the likelihood of achieving the investment’s expected impact

- Identify significant risk factors to the expected impact and seek evidence on the relative size of the challenge addressed in the targeted geographic context

- Consider opportunities to increase impact, and where possible and relevant, indirect and systemic impacts

- Align indicators to industry standards and follow best practices

Overview

Principle 4 focuses on the ex-ante assessment of impact at the individual investment level. It operationalizes an investor’s impact strategy (Principle 1) at the point of investment decision-making and enables robust portfolio-level impact management (Principle 2) with consistent, disciplined investment-level assessment of impact potential. While Principle 4 sets clear expectations for assessing expected impact, it intentionally allows for flexibility so investors can calibrate their approaches based on what is suitable, feasible and relevant, recognizing the varying contexts in data availability, investment strategy and the nature of the underlying problem and solutions.

Under Principle 4, investors are expected to systematically assess and, where possible, quantify the intended impact: who experiences it, how significant it is and how likely it is to be achieved. This includes identifying significant impact risks, grounding assessments in a suitable results framework and using evidence to assess the relative scale of the challenge addressed. Where relevant and possible, investors are also expected to consider opportunities to increase impact, consider indirect and systemic impacts, and align indicators to industry standards and best practices.

Ultimately, Principle 4 ensures impact is not implicitly assumed or retrospectively assessed but instead investigated up front to establish a clear impact rationale before capital is committed. This discipline strengthens decision making, safeguards impact integrity, and enables more effective monitoring, learning and course correction throughout the investment lifecycle.

Challenges in the Implementation of Principle 4

Despite the broad adoption of ex-ante impact assessment, the depth, formalization and consistency of practices vary widely across Signatories. Key challenges include:

- Balancing standardization and contextualization. Investors face a tension between the benefits of using standardized frameworks and metrics for consistency and comparability, and the need to tailor assessments to reflect sector, geography or other specific investment contexts and realities. Over-standardization risks diluting relevance, while overly bespoke approaches limit comparability and portfolio-level aggregation. As noted in Principle 2, many investors address this dilemma by combining standardized impact metrics with tailored investment-specific indicators, as well as by blending quantitative metrics with qualitative narratives. ¹

- Distinguishing outcomes from outputs in ex-ante assessment. Ex-ante assessments often rely heavily on projected outputs and activities, such as customers reached or services provided. These assessments sometimes provide limited insights, however, into how activities and outputs will translate into meaningful outcome-level changes in people’s lives and environmental conditions, grounded in a credible theory of change. Outcome assessment during screening and due diligence remains challenging due to data limitations, uncertainty and complexity in linking activities to real-world results with sufficient evidence.² Where outcome data or evidence is constrained, carefully selected proxies may help ground the ex-ante assessment in clearer impact pathways, while remaining transparent about assumptions and uncertainties.

- Challenges considering indirect or systemic effects. Most Signatories focus their ex-ante assessments on direct impact for primary beneficiaries. Explicit assessment of indirect or system-level effects, such as those relating to value chains, capital market dynamics or broader social or environmental systems, remains a nascent practice. These effects are complex, depend on multiple external factors and contexts, and unfold over long time horizons, making systematic ex-ante assessment and quantification difficult. When included, they are typically addressed through qualitative narratives rather than quantified estimates. This gap highlights a potential area for future methodological development and guidance for the field.³

- Inconsistent assessment of impact risks and likelihood. Few Signatories systematically evaluate the likelihood of achieving expected impact or link it to specific impact risks, mitigation strategies or decision thresholds. This can lead to overstating expected impact when ambition is not calibrated to feasibility, especially for early-stage, innovative or system-level strategies with limited historical evidence. When impact risks are identified, practices vary in depth and structure, with few explicitly using formalized tools such as the ten types of impact risks identified in the Five Dimensions of Impact.⁴ Strengthening practice in this area would improve the credibility of expected impact estimates, clarify underlying assumptions and create a stronger feedback loop for monitoring, learning and improvement under Principles 6 and 8.

- Limited articulation of significance relative to the size of the challenge. While most investors articulate the problem an investment seeks to address and who stands to benefit, few systematically assess how the expected impact compares to the scale of the problem by using market-specific data, evidence or analysis of geographic, sectoral or population contexts. Without this grounding, it is difficult to distinguish incremental from transformational impact potential.⁵

- Resource and data constraints. Many investors — especially those operating in emerging markets, early-stage investments, or nascent thematic areas — face limitations in the availability, reliability and granularity of data needed for robust ex-ante impact assessment. Baseline data are often incomplete, sector-level benchmarks or thresholds may not exist and investees lack the dedicated staff capacity or systems to provide consistent information during due diligence. Even when data is provided, inconsistencies in metric selection and definitions, as well as differences in underlying methodologies and assumptions, can limit comparability across potential investments.

- Difficulty setting realistic impact targets at entry. Even when intended outcomes and KPIs are clearly defined, limited baseline and benchmark data and uncertain operating conditions make it difficult to set credible, time-bound impact targets at the point of investment. As a result, some investors defer target-setting until after investment, when more information can be collected, validated and discussed with investees. Without clear assumptions or a strong linkage to impact risks and investor contribution, impact targets may also become either overly aspirational or insufficiently grounded, undermining their utility for performance management and learning over time. Revising targets over the course of the investment as new and more information becomes available can help targets to be more realistic.

Key Observations in the Implementation of Principle 4

Across disclosure statements, Signatories demonstrate increasing maturity in ex-ante impact assessment practices under Principle 4. While levels of rigor vary, most are moving toward structured and consistent approaches to assessing impact potential to inform investment decisions. Notable observations include:

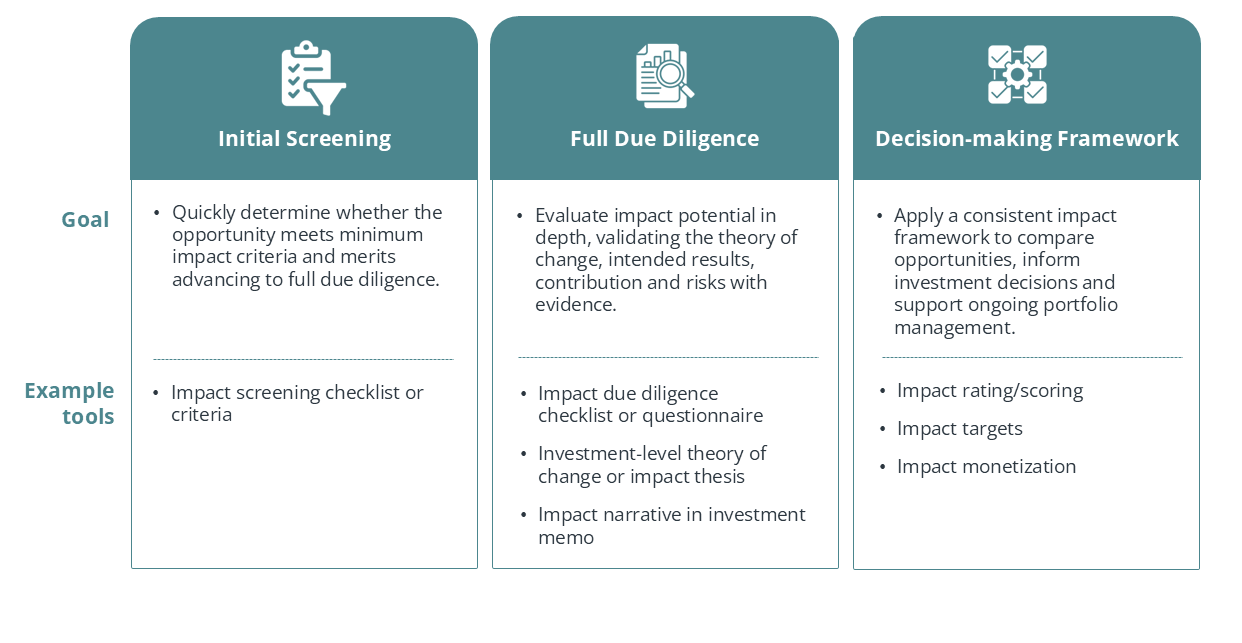

1. Increasing institutionalization of ex-ante impact assessment. Signatories increasingly utilize formalized tools and frameworks to assess impact potential during screening, due diligence and decision-making stages. These tools work together to ensure impact is systematically assessed, documented and integrated into investment decisions, supporting disciplined capital allocation and effective portfolio-level aggregation and management. Common components include:

- Initial screening: Using impact screening checklists or criteria to establish minimum impact alignment and filter out opportunities that do not meet baseline impact requirements before committing full due diligence resources.

- Full due diligence: Assessing expected impact in depth, using a combination of internal and external tools such as impact due diligence checklists or questionnaires, investment-level theories of change and dedicated impact narratives in investment memos.

- Decision-making: Using consistent impact frameworks — such as impact rating, scoring, targets, monetization or quantification — to make impact considerations explicit, systematic and comparable, and to anchor future monitoring and reporting. [See Exhibit 4a.]

Exhibit 4a. Formalized Tools Used in Ex-Ante Impact Assessment

3. Growing use of impact scoring, rating systems and dashboards. An increasing number of Signatories are formalizing ex-ante impact assessment and decision making through structured impact rating or scoring systems. Often integrating the Five Dimensions of Impact and IRIS+, these tools synthesize multiple components of impact considerations into a comparable assessment that can be applied consistently across investments. They help translate qualitative judgements into structured and replicable assessments, reinforcing discipline and consistent decision-making across investments.

In parallel, more investors are using impact dashboards to visualize expected impact across investments and portfolios. Dashboards consolidate ratings, key indicators and thematic or risk exposure in a format that supports portfolio-level analysis, insights and ongoing monitoring and reporting. While methodologies vary, the growing use of ratings and dashboards together reflect a broader market trend toward prioritizing comparability, aggregation and decision-usefulness of impact assessment.

4. Role of theories of change in ex-ante impact assessment. For many Signatories, the theory of change is central in assessing ex-ante impact potential. At the level of a fund, theme, asset class or strategy, theories of change form the foundation of impact frameworks used during due diligence to assess whether prospective investments align with and can credibly contribute to intended impact pathways. Signatories also review or develop investment-level theories of change, which help define appropriate impact metrics and strengthen the robustness of the due diligence process. These may be created by the investee, developed by the investor, or co-created collaboratively. This process brings analytical discipline to understanding how investment activities lead to expected outcomes, articulating evidence-based assumptions, dependencies and impact risks, and evaluating whether an investee’s impact pathway is plausible, measurable and aligned before capital is committed.

5. Quantifying impact potential using KPIs, baselines, thresholds and targets. Many Signatories have moved beyond narrative descriptions to quantify expected impact ex-ante. Notable practices include:

- Selecting key performance indicators (KPIs), often combining standardized metrics (e.g., from IRIS+) with bespoke indicators tailored to the investee’s business model.

- Quantifying impact at multiple levels, including the investment, thematic/sector and portfolio levels.

- Establishing baselines and setting indicative target trajectories to anchor expectations and support future performance monitoring.

- Using thresholds or external benchmarks, which draw on public or sector-specific data, to contextualize both baseline and expected results.

- Formalizing impact targets through agreements, side letters or incentive structures that link targets to management compensation.

Given many challenges related to data availability, consistency and quality, Signatories are adopting adaptive approaches. Some set data requirements at entry and establish or refine baselines within a defined post-investment window (e.g., six to twelve months). KPIs and targets established ex-ante during due diligence may evolve over time post-investment as data systems and collection improve, allowing for flexibility and iterative refinement.

6. Identifying impact improvement opportunities. Some Signatories explicitly identify opportunities to improve impact performance during ex-ante assessment. These may include improving investees’ impact measurement and management systems or enhancing governance, strategy or operational practices to support stronger impact outcomes. Such opportunities may be discussed with investees during due diligence, reinforcing the link between Principle 4 and Principle 3 (investor contribution), and incorporated into post-investment, impact-driven value creation plans. However, fewer Signatories systematically track whether and how these opportunities are implemented and realized over time.⁶

Common, Emerging and Nascent Practices in the Implementation of Principle 4

Note: The findings and observations are primarily based on analysis of the most recent 166 Signatory disclosure statements at the time of the review, published in 2024 and 2025.

An analysis of disclosure statements shows that most Signatories have established systematic approaches to assessing expected impact prior to each investment, reflecting the maturity of ex-ante impact discipline under Principle 4. Common Practices demonstrate how Signatories ground investment decisions in structured frameworks aligned with their impact strategies and theories of change, identify appropriate metrics to quantify and monitor investment-level impact potential, and commonly use IRIS+ and the Five Dimensions of Impact as widely adopted standards and frameworks in impact assessment.

At the same time, disclosures reveal emerging practices that seek to deepen rigor, including impact scoring, impact-related risk assessment and target setting. Nascent practices include the consideration of systemic or indirect impact and the likelihood of achieving expected impact, informed by assessments of impact-related risk factors. Together, these practices illustrate both the significant progress made and the remaining opportunities to strengthen how investors assess investment-level impact potential in a consistent, evidence-informed and decision-useful way across portfolios.

Common Practices

(50 to 100% of disclosures)

- Using an impact framework. 93% of Signatories describe applying a consistent impact framework to assess expected impact at the investment level prior to commitment. About 28% of Signatories include a visual representation of their framework in the disclosure statement, illustrating how impact considerations are systematically applied across investment opportunities.

- Identifying impact metrics or KPIs. 74% of Signatories disclose using impact metrics or KPIs identified through ex-ante impact assessment, with 62% of Signatories citing examples of specific metrics in their disclosures. These metrics, often a mix of standardized metrics and investment-specific indicators, are linked to the theory of change and translate portfolio-level impact goals into measurable indicators at the investment level, forming a basis for post-investment monitoring.

- Aligning indicators to IRIS+. 67% disclose using the GIIN’s IRIS+ to align their impact indicators with a widely adopted industry standard. Around 30% reference using HIPSO or Joint Impact Indicators, particularly among Signatories with development finance organizational mandates or sources of funding.

- Applying the Five Dimensions of Impact. 64% disclose applying the Impact Frontiers’ Five Dimensions of Impact as part of their ex-ante assessment. Some Signatories apply the Five Dimensions directly, while others use adapted or integrated versions embedded within proprietary impact frameworks or standards.

Emerging Practices

(25 to 50% of disclosures)

- Impact scoring or rating. 44% disclose using a formalized impact scoring or rating approach within their impact frameworks to support consistent assessment and comparison across potential investments during screening or due diligence processes.

- Identifying impact risk factors. 35% disclose identifying and considering impact-related risks that cause actual impact to vary from expectations.

- Considering the relative size of the challenge. 28% disclose considering or assessing the relative scale of the problem being addressed, often through discussions of local, country-level, regional or global contexts.

- Setting impact targets. 27% disclose establishing explicit impact performance targets at the investment level, which are monitored and may be reassessed over the course of the investment period.

Nascent Practices

(<25% of disclosures)

- Indirect and systemic impact. 19% disclose considering indirect and systemic impact, extending beyond direct outcomes experienced by immediate beneficiaries to include broader market, sectoral, value chain or ecosystem-level effects associated with an investment. When mentioned, these considerations are typically narrative-based rather than quantified as indicators.

- Use of third-party advisors. 19% disclose using external advisors or specialists to support impact assessment, particularly where internal capacity or sector expertise is limited. Advisors may contribute to impact framework design, due diligence or in-depth sector-level or technical expertise during the assessment process.

- Assessing likelihood of achieving expected impact. 16% disclose assessing the likelihood of achieving expected impact, going beyond identifying risks to explicitly consider feasibility or probability. Assessments are typically qualitative rather than quantitative.

- Use of third-party data. 15% disclose using external data for assessing expected impact, including public data sources from international, government or academic agencies, as well as sector benchmarks or other specialist research data. These data are typically used to contextualize impact assessments and assumptions.

- Impact dashboard. 14% disclose using an impact dashboard to consolidate and compare, analyze and communicate impact data across their investments.

- Impact monetization or valuation. Only 2% of Signatories disclose using impact monetization or valuation approaches, translating impact outputs or outcomes into a monetary value to allow comparison across investments.

Principle 4 Signatory Practice Spotlights

-

Asset Class: Infrastructure

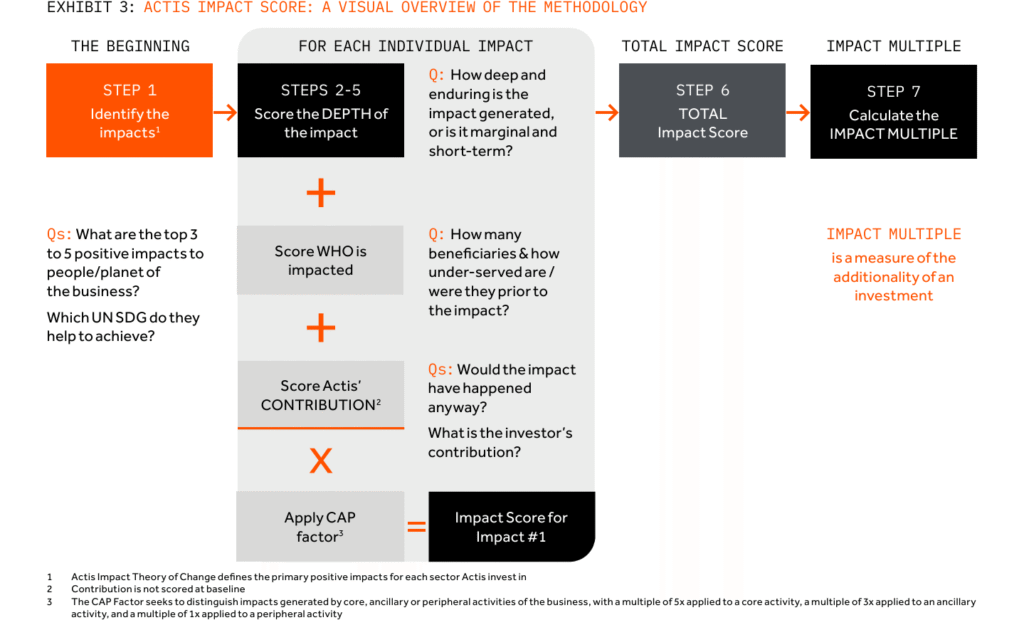

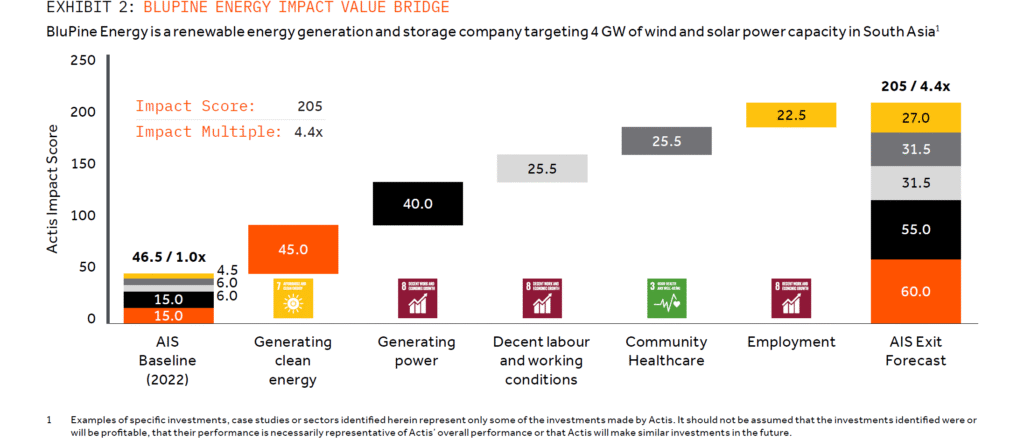

Actis is a leading growth market investor in sustainable infrastructure. It invests in structural themes that aim to support long-term, equitable growth in defensive, critical infrastructure across energy transition, digitalization transition and supply chain transformation. Actis integrates ex-ante impact assessment directly into investment decision-making through its proprietary Actis Impact Score (AIS), a tool used to measure and monitor impact performance on a portfolio basis.

- The Actis Impact Score (IAS): The AIS estimates the projected impact outcomes of a prospective investment and reflects a transaction-specific impact thesis. These forecast scores are jointly developed by the investment and sustainability teams ahead of Final Investment Committee approval to define the intended impact of the proposed investment the beneficiaries, and the magnitude of impact targeted. Prior to deal completion, investments receive a forecast AIS score, translating an investment’s impact thesis into quantified projections and visually mapping expected outcomes through an Impact Value Bridge. [See practice examples 4.1 and 4.2.]

- Needs-based impact assessment: Actis evaluates impact potential using the Five Dimensions of Impact and integrates country- and market-level data from credible global sources (e.g., ILO, World Bank, WHO) to assess the extent to which targeted beneficiaries are underserved and to contextualize the anticipated contribution of the investment.

- Linking risk-adjusted projections to monitoring and value creation: AIS incorporates a baseline assessment of the likelihood of achieving intended impact. These insights guide portfolio monitoring and engagement, helping Actis target risk mitigation actions and strengthen delivery of both direct and indirect impacts.

- Standardized impact performance tracking using common indicators: Indicators draw on industry standards such as the SDGs, IRIS+ and Joint Impact Indicators where possible to quantify and track investment-level impact potential and outcomes consistently across investments.

Practice Example 4.1

BNPP Social Business Impact – Contribution

Practice Example 4.2Visualizing Expected Impact Through the AIS Impact Value Bridge

Asset Class: Multi-Asset Class (Private Debt, Fixed Income and Private Equity)

BlueOrchard, a member of the Schroders Group, manages the largest microfinance fund globally and serves as a trusted partner to leading development finance institutions through its expertise in blended finance mandates. It conducts ex-ante impact assessment through its proprietary B.Impact Framework, which applies standardized sustainability and impact scorecards and ratings across impact themes and asset classes (private debt, private equity and listed debt). [See Practice Examples 4.3.]

- Impact Framework – a standardized impact management framework: As part of the framework, each prospective investment undergoes a structured Impact Scorecard assessment prior to selection and must meet a defined minimum impact score and be approved by the impact management team to be eligible for portfolio inclusion. [See Practice Examples 4.4.]

- Structured assessment aligned with the Five Dimensions of Impact: The structured Impact Scorecard assesses each investment opportunity following the Impact Frontiers’ Five Dimensions of Impact. It combines analysis of impact intent KPIs and target stakeholder information with assessment of fund- and investee-level contribution, while accounting for potential unintended negative effects and risks that the intended impact may not be achieved.

- KPIs aligned with industry best practices: Impact KPIs are mapped to the SDGs and, where possible, aligned with widely accepted standards, including IRIS+, IFC Performance Standards, ICMA and HIPSO, to support consistent measurement across investments and asset classes.

- Scoring linked to portfolio monitoring and governance: Impact scores are aggregated and tracked at the portfolio level and regularly communicated to senior management, fund boards and investors to inform performance monitoring and oversight.

Practice Example 4.3

BlueOrchard’s Proprietary B.Impact Framework

Practice Example 4.4

BlueOrchard Impact Scorecard for Investment Impact Assessment

Important information

Marketing material.

The information in this document was produced by BlueOrchard Finance Ltd (“BOF”), part of Schroders Capital which refers to those subsidiaries and affiliates of Schroders plc that together comprise the private markets investment division of Schroders. It may not be distributed or reproduced by the recipient without express written consent of BOF. BOF has outsourced the provision of IT services (operation of data centres, data storage, etc.) to Schroders group companies in Switzerland and abroad. A sub-delegation to third parties including cloud-computing service providers is possible. The regulatory bodies and the audit company took notice of the outsourcing and the data protection and regulatory requirements are observed. For information on how BOF and the Schroders Group may process your personal data, please view the BOF Privacy Policy available at www.blueorchard.com/legal-documents/ and the Schroders’ Privacy Policy at https://www.schroders.com/en/global/individual/footer/privacy-statement/ or on request should you not have access to these webpages.

Issued by BlueOrchard Finance Ltd, Talstrasse 11, CH-8001 Zurich, a manager of collective investments authorised and supervised by the Swiss Financial Market Supervisory Authority FINMA, Laupenstrasse 27, CH-3003 Bern.

© 2026, BlueOrchard Finance Ltd. All rights reserved.

Asset Class: Private Equity

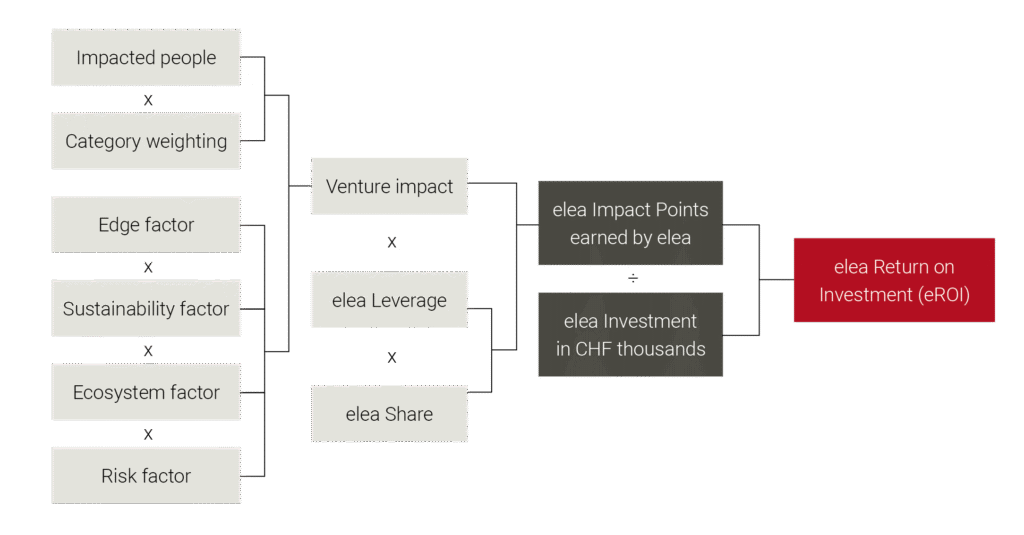

The elea Foundation for Ethics in Globalization is a philanthropic impact investor dedicated to fighting absolute poverty with entrepreneurial means. Through a mix of equity, loans, and grants, elea provides catalytic capital to help investees scale their operations and increase their impact. Its ex‑ante impact assessment is grounded in the elea Impact Measurement Methodology (eIMM), a proprietary framework that translates expected impact into elea Impact Points, enabling comparison of impact potential across diverse business models. [See practice example 4.5.]

- Quantifying venture impact using impacted people weighting and multipliers: At the core of the eIMM is the calculation of venture impact, which begins by estimating the number of impacted people – both directly and indirectly reached. The impacted people are allocated to one of nine categories with specific weightings that reflect differences in the intensity and continuity of expected benefits, as pre-defined by distinct theories of change. To capture the composite venture impact, the weighted impacted people figure is then multiplied by a series of factors, including:

- Edge factor: captures the venture’s innovation and level of transferability

- Sustainability factor: evaluates financial viability and execution capacity

- Ecosystem factor: weighs the ability to build or strengthen an ecosystem that increases its impact on people living in absolute poverty

- Risk factor: considers political, environmental, cultural and thematic risks motivating the use of philanthropic capital

- Incorporating investor contribution through elea Share and elea Leverage: elea then reflects its monetary and non-monetary contributions into the final score through the elea Share, its portion of the total funding, and the elea Leverage, the extent of its non-financial contribution. The product of venture impact with these figures yields elea Impact Points, an artificial currency that allows elea to compare impact potential on a standardized, consistent basis.

- Operationalizing impact assessment: elea uses the eIMM not only to support its investment selection process, but also to set ex-ante impact targets which are measured against annually. By aggregating elea Impact Points across active investments, elea also monitors impact performance consistently at the portfolio level, supporting learning and prioritization for investee engagement throughout the investment lifecycle.

Practice Example 4.5

elea’s eIMM Methodology

Asset Class: Private Debt / Alternative Credit

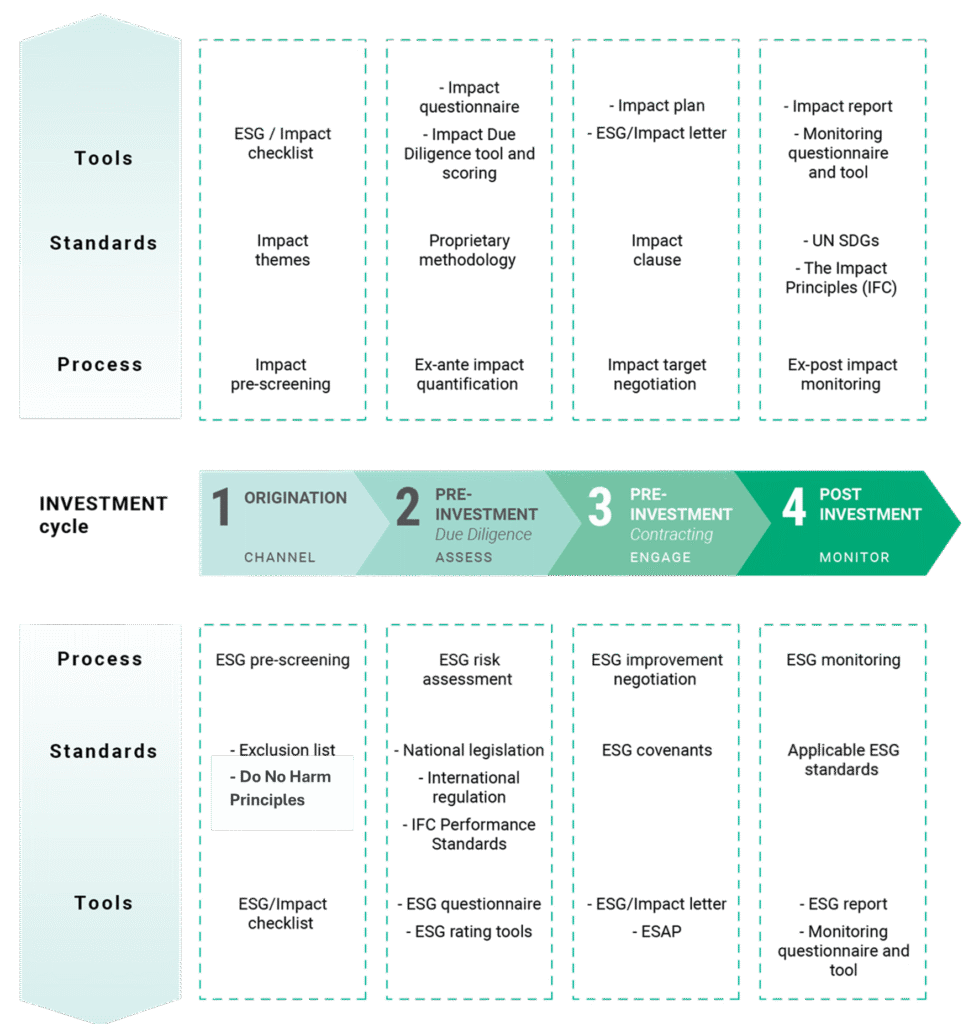

INOKS Capital is a Swiss asset manager specializing in customized financing solutions for companies primarily in the agriculture and food sector in fast-developing markets in Sub-Saharan Africa, Asia, Latin America and Europe. INOKS Capital aims to expand access to capital for resilient, value-adding activities within the real economy. To assess the expected impact of investments, INOKS Capital has established a structured methodology applied consistently across the pre-investment process. [See Practice Example 4.6.] In practice, this approach is applied across three main steps:

- Origination – Systematic sourcing using a proprietary database: Investments are sourced using a proprietary database identifying high-impact Areas (HIAs) and high-risk areas (HRAs) at the country, commodity and value chain levels. This provides a preliminary view of priority opportunities by addressing country-specific development needs (e.g., access to finance, food security) while identifying areas with elevated environmental and social risks.

- Screening – Establishing initial impact alignment: Potential investees undergo initial screening to assess expected impact and evaluate their contribution to INOKS Capital’s four impact themes — poverty reduction, food security, environmental quality and women’s empowerment — as well as to its long-term objective of developing sustainable agricultural value chains.

- Due Diligence – Conducting full ex-ante impact quantification: A comprehensive impact and risk assessment integrates contextual analysis with ex-ante impact quantification under INOKS’ Impact Measurement Framework. Investments are assessed using both IRIS+ and in-house indicators, contributing to an impact score to assess investees’ contribution to each impact theme. The impact analysis findings are formalized in an Impact Factsheet. Identified improvement opportunities are discussed with the investee, and expected impacts, including measurable quantitative targets, are incorporated into the engagement letter.

Practice Example 4.6

INOKS’ Ex-ante Impact Assessment Approach

Asset Class: Private Equity

Lightrock is a global sustainable investment platform operating across public and private markets. Its private-market impact investing focuses on scaling growth-stage companies across three themes: people, planet and productivity/tech for good. Within these themes, Lightrock focuses on specific sectors or subthemes and develops impact objectives and evidence-based theories of change for each.

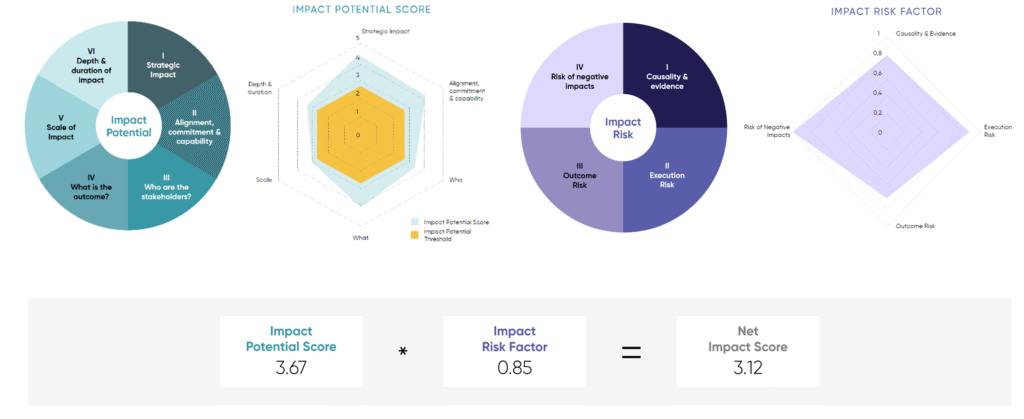

For each investment, Lightrock assesses expected impact using two complementary proprietary tools: the Lightrock Impact Scorecard, which quantifies risk-adjusted impact potential, and the Impact Model, which defines the impact narrative, including the impact rationale, expected outcomes and KPIs.

- Quantifying risk-adjusted impact potential: The Lightrock Impact Scorecard turns qualitative assessments of impact potential and risks into a standardized, quantitative impact score. Drawing on the Five Dimensions of Impact, the tool evaluates expected impact across six categories and aggregates the results into a single Impact Potential Score. This score is adjusted using an Impact Risk Factor that assesses impact-related risks across four categories. The outcome is a risk-adjusted net impact score that provides a holistic, consistent and comparable view of each opportunity’s positive impact potential to support informed investment decision-making. [See Practice Example 4.7.]

- Developing the impact narrative: Lightrock’s Impact Model complements the Impact Scorecard by supporting investment managers to further develop the impact rationale behind a prospective investment. This includes detailing the expected outcomes and the underlying theory of change with evidence for both the relative size of the challenge and the effectiveness of the proposed solution.

- Defining KPIs and setting targets: Using insights from the Impact Model, investment managers identify relevant impact KPIs, typically drawing on standardized metric sets like IRIS+ and the Joint Impact Indicators. KPIs are systematically tracked and monitored. Where appropriate, impact targets are established for selected KPIs and incorporated into ongoing performance management. The approach to target setting may vary at the investment or portfolio level depending on the strategies and investments.

Practice Example 4.7

Lightrock’s Proprietary Impact Scorecard

Asset Class: Private Equity

Mediterrania Capital Partners (MCP) is a private equity firm focused on growth investments in small and medium enterprises (SMEs) and mid-cap companies across Africa, with a focus on value creation and sustainable development. MCP supports sectors that directly enhance people’s well-being and promote inclusive growth, including healthcare, pharmaceuticals, medical equipment and diagnostics, and financial inclusion.

MCP’s ex-ante impact assessment balances standardized metrics with tailored impact criteria, grounded in a clear impact thesis for each prospective investment. A proprietary scoring tool quantifies expected impact potential as well as associated risks to inform decision making and anchors post-investment monitoring and value creation plans.

- Impact thesis for each investment: Each prospective investment includes a specific impact thesis articulating anticipated impact outcomes, aligned with a structured theory of change and identifying relevant SDG targets, 2X Challenge criteria (where applicable), and sector-specific impact themes.

- Standardized and sector-specific metrics: Core indicators from the IRIS+ catalog serve as a baseline for assessing all investments, supplemented with sector-specific metrics tailored to industries and investment-specific KPIs capturing each investee’s unique contribution to impact creation.

- Tailored impact criteria: In addition to standardized metrics, MCP applies tailored impact criteria that reflect the specific sector, business model and impact pathways of each prospective investment. This allows MCP to evaluate the impact dimensions that are most material to each investment, while preserving a level of comparability across the portfolio through a common scoring framework.

- Ex-ante impact scoring linked to capital allocation: Prospective investments receive an impact score prior to approval, refined following environmental and social due diligence and benchmarked across the portfolio. The scorecard assigns both numerical (0-100) and letter grades (D to A+), where higher scores indicate stronger expected impact performance and management systems, and higher ratings reflect greater robustness in data quality, governance, accountability and transparency.

Asset Class: Private Equity and Private Debt

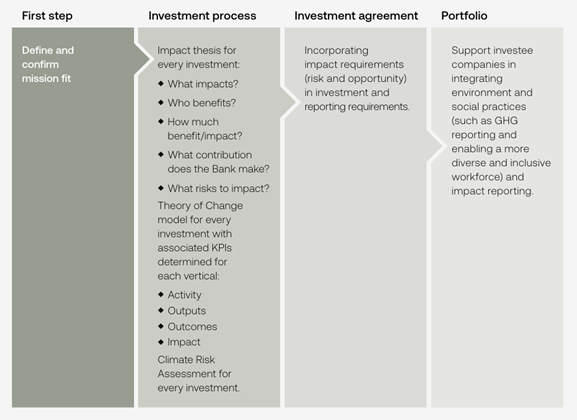

The Scottish National Investment Bank is a development investment bank established by Scottish Ministers to deliver impact across three national priorities: net zero, places and communities, and innovation. The bank applies a structured impact assessment framework from origination through portfolio management, using mission fit, impact scoring, theories of change and KPIs to guide investment decisions and track progress. [See Practice Example 4.8.]

- Mission-aligned screening and thesis development: All investment proposals are screened at initial enquiry for mission alignment and assessed using the Five Dimensions of Impact to develop bespoke impact theses. This identifies the type and scale of expected impact, target beneficiaries, expected contribution and risks to impact delivery. All investments are assigned low-to-high impact ratings to support consistent comparisons across the pipeline.

- Multi-level KPIs with baseline driven by theory of change: For each investment, the Bank co-creates an investment-level theory of change with the investee, capturing expected activities, outputs, outcomes, and mission impact. The theory of change establishes mutually agreed impact KPIs that reflect the investment’s specific pathway to impact. Impact KPIs are applied at the investment, mission and portfolio levels, with baselines established at the point of investment, providing a foundation for ongoing monitoring. [See Practice Example 4.9.]

- Assessing and scoring investor contribution: The bank assesses and scores its expected contribution using a structured model based on three dimensions:

- Financial additionality: Providing capital where capital is not available, or not available in sufficient quantity or terms.

- Value additionality: Knowledge, advice, governance and impact expertise.

- Mobilization: Enabling co-investment by other investors.

The bank then scores its contribution using a combined view of confidence (likelihood of providing additional value) and scale (assessment of “value add”).

Practice Example 4.8

The Scottish National Investment Bank’s Approach to Impact Assessment

Asset Class: Multiple

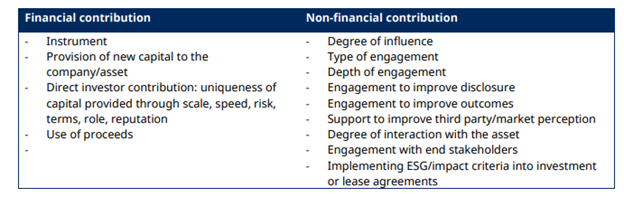

Schroders is a global asset manager with a range of impact-driven strategies across listed equity, listed debt, private equity, real assets, and multi-private asset solutions. Leveraging proprietary tools and an independent impact governance committee, Schroders applies a systematic impact framework across its diverse portfolio, drawing on the expertise of BlueOrchard. Central to its approach is a commitment to investor contribution through both financial and non-financial means, which is systematically assessed through a proprietary impact scorecard and pursued through structured approaches to active ownership and engagement.

- Assessing contribution through a proprietary impact scorecard: Schroders assesses its contribution for each transaction, using a bespoke impact scorecard that draws on Impact Frontiers’ 5 Dimensions of Impact. To isolate the nature of its contribution for each investee, the firm assesses both financial and non-financial contribution across a number of categories. [See Practice Example 3.5.]

- Active engagement across asset classes: Schroders emphasizes the need for active engagement that is tightly aligned with impact intent, supports improved impact measurement, and contributes directly to impact outcomes. The firm publishes “Engagement Blueprints” that outline its ambitions, priorities, and expectations for active ownership across public and private markets, identifying and employing the specific levers available to it by asset class. [See Practice Example 3.6].

- Tracking engagement systematically: Schroders tracks the effectiveness of its engagement activities through a proprietary active ownership tool called “Active IQ,” focusing on forward-looking engagement plans and a milestone-based progress tracking system.

Practice Example 3.5

Schroders’ financial and non-financial contribution categories

Practice Example 3.6

Schroders’ approach to listed equity active ownership

Asset Class: Multi-Asset Class

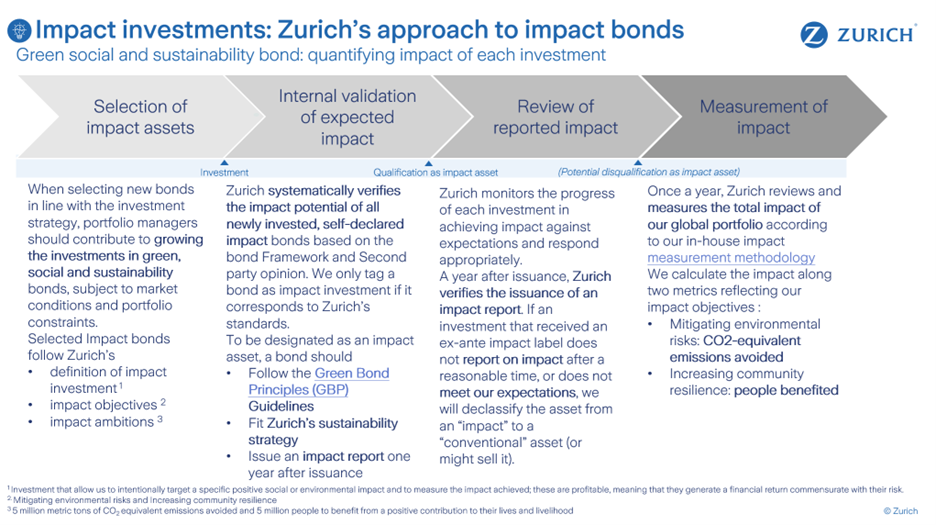

Zurich Insurance Group is a global insurer that centers its impact investing approach on two priorities: mitigating environmental risks and increasing community resilience. As a diversified institutional asset owner, Zurich Insurance‘s impact investment portfolio is allocated to use-of-proceeds bond, impact private debt fund, and impact private equity fund. In assessing an investment’s expected impact, Zurich Insurance takes a systematic approach that is both grounded in its own impact objectives and tailored to differences across asset classes.

- Systematic impact assessment: Zurich assesses expected impact by evaluating an investment across three categories. It analyses the “what” to identify the intended impact of a given investment in line with Zurich’s impact objectives, the “who” to identify beneficiaries, and the “significance of impact” to assess its pro-rata share of the impact achieved by an investment. The metrics are aligned with industry standards such as IRIS+.

- Asset‑class–specific practices: In addition to its standardized approach, Zurich tailors its impact assessment to each asset class’s particular characteristics.

- Fixed income (green, social and sustainability bonds): Assesses the ex‑ante impact potential of financed projects, while evaluating the issuer’s intent and the project’s alignment with its sustainability strategy.⁸ [See Practice Example 4.10.]

- Impact infrastructure private debt: Applies the Green and Social Bond Principles categorization, differentiating between environmental and social impact infrastructure, and requires non‑financial reporting from project developers.

- Impact private equity: Evaluates fund managers’ strategies by theme, customer segment, sector and geography, requiring commitment to impact reporting but not an explicit impact fund branding.

Structured foundation for portfolio‑level aggregation: Zurich’s ex‑ante assessment methodology feeds directly into its broader impact measurement system⁹, allowing aggregation of impact data across asset classes and progress towards its ambition to help to avoid 5 million metric tons of CO2e emissions per year and contribute to benefiting 5 million people annually.

Practice Example 4.10

Zoom into Zurich’s Bonds Impact Assessment

The unique characteristic of green, social and sustainability bonds is the pre-defined use of proceeds according to criteria to which issuers commit, clearly linking the investment to specific projects that allow the bond issuer to report a result or impact. When analyzing use-of-proceeds bonds and deciding whether they should be classified as impact instruments, Zurich focuses primarily on the projects to be financed, and their ex-ante potential for positive impact.

Footnotes

¹ Also read on challenges related to data quality and standardization of metrics in the Principle 8 Common and Emerging Practices.

² Also read on challenges related to measuring outcomes versus outputs in the Principle 8 Common and Emerging Practices.

³ The Systems Thinking for Impact Investing Primer and Playbook published by the Rockefeller Philanthropy Advisors and Shift Systems Initiative offer practical frameworks and toolkits for applying systems thinking to impact investing practice, including how it can be integrated with the Impact Principles.

⁴ https://impactfrontiers.org/norms/five-dimensions-of-impact/impact-risk/

⁵ The GIIN’s COMPASS methodology introduces a structured approach for interpreting the significance of expected results by comparing impact results relative to peers and magnitude of the corresponding social or environmental challenge.

⁶ Read more on investor contribution in Principle 3 Common and Emerging Practices.

⁸ Read a case study on Zurich’s investment in the City of Zurich Green Bond

⁹ Learn more on Zurich’s impact measurement framework in its methodology paper.