Introduction

The Common and Emerging Practices, a new series of resources from the Impact Principles, aims to capture key insights from notable trends in common practices in implementing the Impact Principles by our Signatories and highlight promising emerging practices and key gaps. By sharing these common and emerging best practices in impact management, we seek to elevate impact practice in the market and ensure that capital is mobilized at scale with integrity to drive meaningful impact outcomes.

The resources related to Common and Emerging Practices will be released in phases through website publication of initial drafts for each of the nine principles in series, followed by draft and final consolidated reports with stakeholder engagement.

Principle 2

Manage strategic impact on a portfolio basis

The Manager shall have a process to manage impact achievement on a portfolio basis. The objective of the process is to establish and monitor impact performance for the whole portfolio, while recognizing that impact may vary across individual investments in the portfolio. As part of the process, the Manager shall consider aligning staff incentive systems with the achievement of impact, as well as with financial performance.

The Components of Principle 2

- Have a process to manage impact achievement on a portfolio basis

- Establish and monitor impact performance for the whole portfolio, while recognizing variance across individual investments

- Consider aligning staff incentive systems with the achievement of impact, as well as with financial performance

Overview

Principle 2 calls attention to systems and processes that enable investors to implement impact objectives across their portfolios with institutional discipline and consistency. It emphasizes the need for investors to manage and monitor impact performance at the portfolio level, rather than solely at the level of individual investments. This approach helps investors gain a holistic view of their investments and track their performance and contributions with the goal of optimizing portfolio-level outcomes.

Importantly, as part of this process, Principle 2 also encourages managers to align staff incentive systems with impact achievement, embedding impact considerations into organizational decision-making and reinforcing accountability.

Challenges in the Implementation of Principle 2

Managing impact at a portfolio level requires organizational commitment and investment into systems, processes and capacity to be effective in the long-term. In doing so, investors face a number of challenges:

- Managing impact performance across diverse portfolios. Establishing and monitoring portfolio-level impact performance can be complex when the underlying investments may target different impact themes and outcomes or include a mix of asset classes, geographies, direct and indirect investments, and investment stages. This may be the case across multiple funds or within a single fund for different investor contexts. This diversity complicates efforts to establish a manageable set of standard impact metrics, aggregate across investments, and assess and compare performance across a portfolio.

- Challenges in analyzing and comparing impact performance. In recent years, meaningful progress has been made in the development of tools, resources and market infrastructure to assess and compare impact performance.1 However, challenges remain, including a fragmented landscape of tools, inconsistent data definitions and methodologies, and limited willingness and capacity among investors to share data at the level needed for robust benchmarking and portfolio-level impact performance analysis.

- Siloed impact and financial management. For many impact investors, impact management remains siloed from financial management, with separate teams, results frameworks, processes, systems and reporting. This isolated approach compromises opportunities to better understand and monitor the impact and financial returns of the portfolio in a holistic manner, and to optimize both impact and financial performance in portfolio construction and management across the investment lifecycle.2

- Lack of direct control when investing in funds (e.g., fund-of-funds). Operating through fund-of-funds structures or allocating capital to external managers can complicate portfolio-level impact management, with such investors having limited influence on underlying investments. In these cases, impact accountability is distributed across multiple layers, and impact practices vary from manager to manager. These investors, as limited partners, can influence portfolio impact management and performance of managers by aligning on impact standards, frameworks and incentive structures as part of their due diligence and selection process and setting of deal terms — including side letters or Limited Partner Agreements — as well as by providing capacity-building support.3

- Complexity in implementing impact-aligned staff incentives. Establishing and operationalizing staff incentive structures aligned with impact can be complex for a number of reasons:4

- Setting metrics and targets: One major hurdle is selecting appropriate metrics to base incentives on that are material to the fund’s impact objectives while sufficiently measurable and verifiable. Setting ambitious yet realistic targets can be especially challenging when there is limited data available on baseline, threshold or peer benchmarks.

- Aggregating performance: Aggregating impact performance at the portfolio level can pose additional challenges with data quality and variances in the methods and cadence of data collection. This can be true for both standardized and tailored metrics.

- Governance and administration: It is not straightforward to design and implement the right mechanisms and governance to operationalize incentive structures, with investors needing to strike the right balance between flexibility and accountability. There can also be significant operational burdens related to documenting, monitoring and administering these incentive systems.

- Unintended consequences: Investors risk creating unintended negative consequences due to overly simplistic structures or misaligned incentives that change how investors make portfolio management decisions. A related issue is cherry-picking specific metrics or investments that present impact performance in a more favorable light.

Key Observations in the Implementation of Principle 2

Signatories are advancing their practices to manage strategic impact at the portfolio level by building structured policies, systems and processes that embed impact management across diverse portfolio contexts. They are institutionalizing portfolio-level impact practices through integrated frameworks, standardized tools, dedicated governance, aligned incentives and enabling technologies. These evolving practices reflect a growing maturity in how investors define, assess and manage impact at scale — balancing standardization with contextual flexibility and adapting organizational structures to support credible impact management practices across complex portfolios.

Notable observations include:

1. Building systems for portfolio-level impact management. By becoming a Signatory to the Impact Principles, an investor already commits to integrating impact across the investment lifecycle. Some Signatories further demonstrate how they institutionalize impact management by clearly mapping their impact processes, related frameworks, tools and responsibilities at each investment stage. They may include standardized impact screening and monitoring tools, analytical frameworks, technology-enabled data systems, formalized impact-related policies and governance, and dedicated or integrated in-house impact teams, often supplemented by outsourced expertise. Standardizing impact management throughout the investment lifecycle enables robust implementation of impact strategy across the portfolio and promotes effective continuous learning and improvement as an organization.

2. Various portfolio contexts and structures. Signatories to the Impact Principles operate across a wide spectrum of portfolio contexts and investor types, which shapes how they manage impact at the portfolio level. The majority are asset managers raising and deploying dedicated capital through one or more impact strategies or funds. These include impact-focused firms whose entire assets under management (AUM) are dedicated to impact, as well as mainstream managers, whose impact offerings represent a small portion of a broader investment platform. Some Signatories are asset owners with specific impact objectives applied to their total portfolio or a carved-out allocation. Others are allocators – such as wealth managers or investment advisors – who oversee diverse portfolios tailored to varied client preferences. In these cases, managing impact performance often requires a broader and more flexible approach, with different metrics, aggregation methods, and reporting tools than those used by managers of focused impact funds. These distinctions underscore the importance of considering investor type and portfolio composition when implementing Principle 2, as practices in impact management will necessarily vary depending on structure, strategy and level of control. [See Exhibit 2a.]

Exhibit 2a. Various Portfolio Contexts Influencing Portfolio-level Impact Management Practices

4. Enabling technology and tools. Signatories are becoming more sophisticated in how they integrate impact measurement data into their portfolio management systems, shifting from fragmented, ad hoc or manual impact tracking toward more institutionalized, technology-enabled systems. These platforms enable real-time, portfolio-wide impact analysis and oversight, as well as integration with broader investment and risk-related data or business processes for more holistic decision making. [See Exhibit 2b.] Some Signatories and verifiers are exploring using AI tools and automated analytics to enhance their impact intelligence or amplify impact and value creation among their portfolio companies.

Exhibit 2b. Leveraging Technology and Tools for Portfolio Impact Management

6. Managing impact across diverse and multi-asset portfolios. Signatories are increasingly adopting systematic approaches to manage impact across multiple impact themes, sectors and asset classes, reflecting the growing maturity of Principle 2 implementation as well as the flexible applicability of the Impact Principles. Investors turn the organizational challenge of managing complex, diversified impact portfolios into a strength by ensuring clear strategic alignment, unified impact frameworks, cross-portfolio management tools and appropriate governance and capacity. [See Exhibit 2c.]

Exhibit 2c. How Investors Manage Impact Across Diverse and Multi-asset Portfolios

Exhibit 2d. Common Models for Aligning Incentives with Impact

Common, Emerging and Nascent Practices in the Implementation of Principle 2

Note: The findings and observations are primarily based on analysis of the most recently published 166 Signatory disclosure statements at the time of the review in early to mid-2024.

There is a wide range in what and how Signatories disclose regarding their alignment with Principle 2. Many provide comprehensive descriptions of how impact is embedded across the entire investment lifecycle, including pre- and post-investment phases, along with details on portfolio-level impact metrics, frameworks and monitoring systems. The majority of Signatories confirm aligning staff incentives with impact, while others are still considering aligning incentives as best practices emerge. The majority of Signatories also discuss governance or team structures as part of organization-wide systems that enable portfolio-level impact management.

No emerging or nascent practices were identified for Principle 2– likely reflecting both the relative maturity of current implementation practices and the broad, overarching nature of the Principle itself.

Common Practices

(50 to 100% of disclosures)

- Managing impact at a portfolio level. 100% of Signatories confirm or describe managing impact at a portfolio level. The description is typically accompanied by portfolio-level impact goals or metrics, impact frameworks, or systems and processes for the consistent assessment and monitoring of investments.

- Impact management process across the investment lifecycle. 87% of Signatories describe how impact is systematically managed throughout the investment lifecycle across the portfolio, sometimes including a helpful graphic illustration of the streamlined process.

- Portfolio-level impact metrics. 72% of Signatories disclose having portfolio-level impact metrics that are regularly tracked and aggregated across investments, while 94% mention having indicators at any level, including for individual investments. Additionally, 62% provide examples of specific metrics or key performance indicators used to manage impact performance across the full portfolio or toward particular impact objectives. Signatories use a combination of standardized metrics – often aligned with frameworks such as IRIS+ or HIPSO – and bespoke indicators tailored to specific investment contexts.

- Aligning staff incentives with impact achievement. 67% confirm that they align staff incentives with impact. The alignment with impact often includes qualitative as well as quantitative measures, and the approach may vary by investor type or asset class. Common approaches include impact-linked carry, bonuses and performance evaluation. An additional 30% of Signatories disclose considering aligning incentives in the future as best practices emerge.

- Governance: Policies and Committees. 62% of Signatories disclose information on formal impact-related policies or committee structures that support impact management and decision making. Approaches vary: some embed impact-related oversight into existing investment policies or investment committee mandates, while others establish dedicated mechanisms such as impact-specific policies or impact advisory committees.

- Organizational structure and team capacity. 53% of Signatories disclose information on how they structure internal capacity to support impact management. This includes dedicated in-house impact teams, investment teams with integrated impact responsibilities, and the use of external advisors or third-party evaluators.

Emerging Practices

(25 to 50% of disclosures)

None identified at this time for Principle 2

Nascent Practices

(<25% of disclosures)

None identified at this time for Principle 2

Principle 2 Signatory Practice Spotlights

-

Asset Class: Private Equity / Venture Capital

Accion is a global nonprofit organization focused on advancing a more inclusive economy by expanding access to financial services for underserved populations, including women, smallholder farmers and Micro, Small, and Medium Enterprises (MSME). Impact considerations are embedded into decision-making at each stage, supported by a proprietary impact framework, centralized data systems and incentive structures that reinforce alignment across teams.

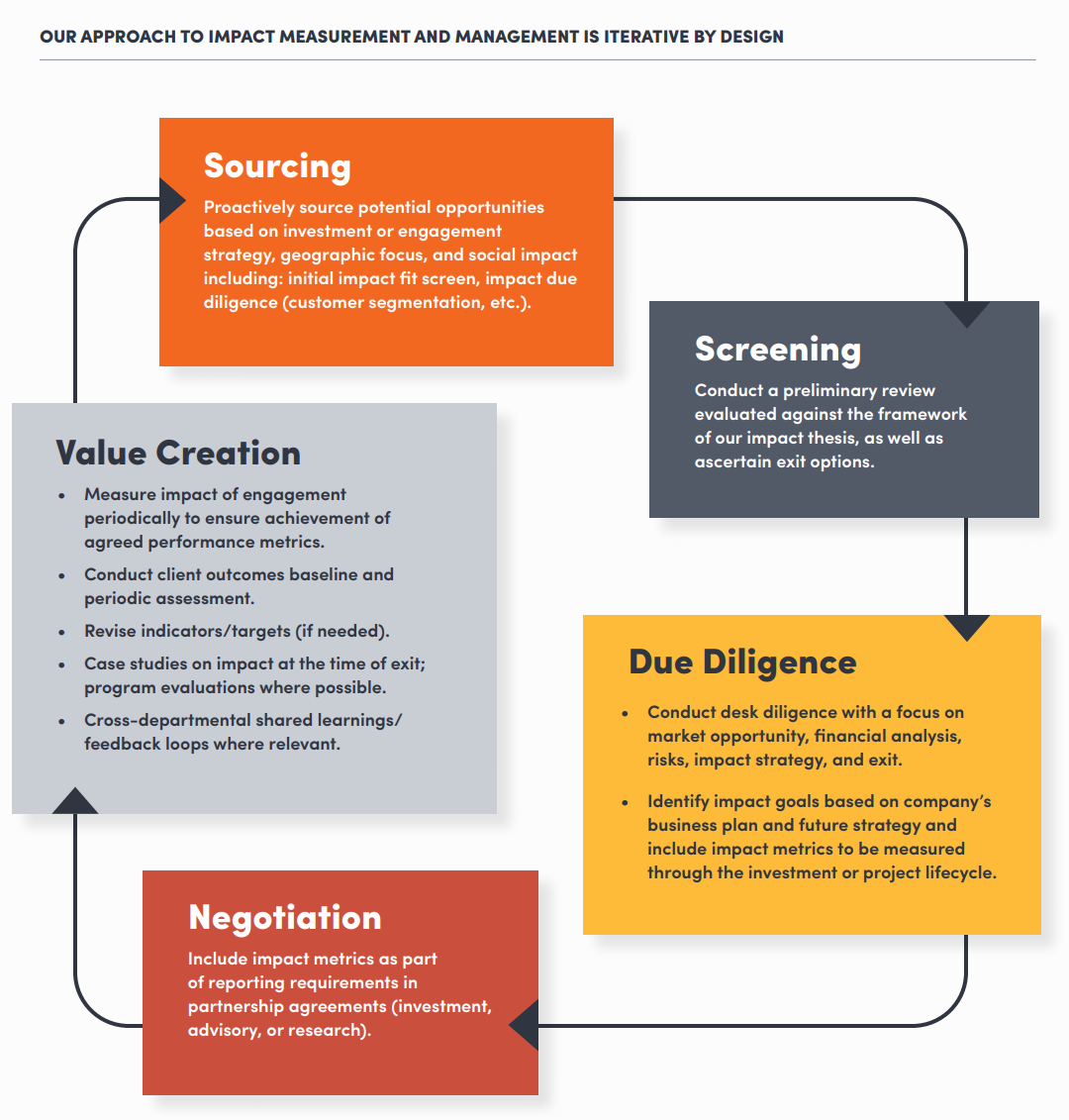

- Embedding impact across the investment life cycle: Accion integrates impact into every stage of the investment process in a disciplined, systematic way — from early screening to due diligence to value creation. During due diligence, investment teams develop an impact thesis that assesses how the company’s mission, customer base and business model align with the fund’s strategic objectives. [See Practice Example 2.1.]

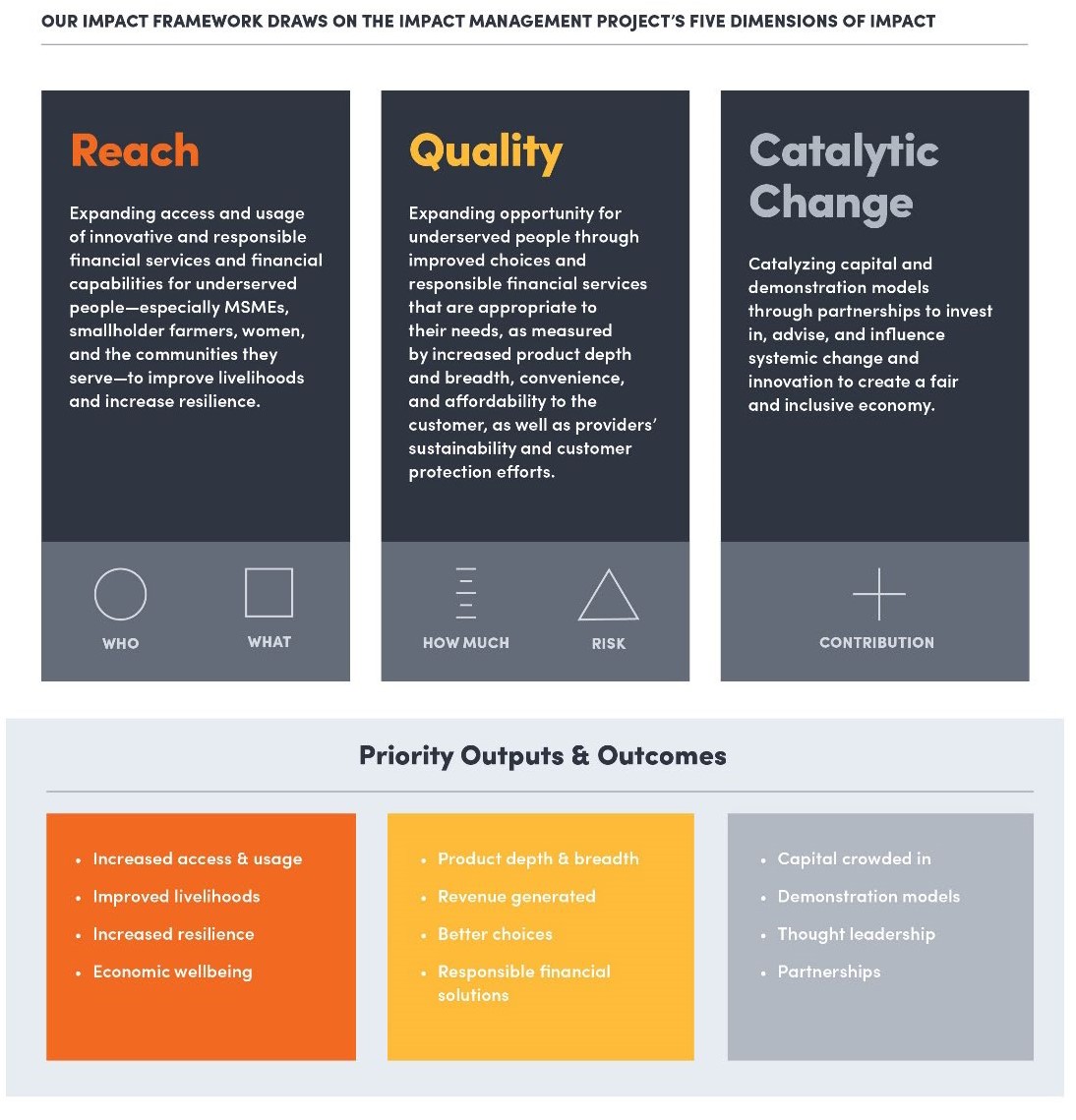

- Applying a structured portfolio framework: Accion’s impact framework tracks outcomes across three dimensions — reach, quality and catalytic change — using KPIs aggregated annually. Fund-level and company-specific indicators align with IRIS+ and the SDGs where relevant, enabling consistency across the portfolio. [See Practice Example 2.2.]

- Tech-enabled data aggregation: Each quarter, investment teams aggregate datasets of operational and impact indicators from all active portfolio companies using customized portfolio monitoring software. These datasets include metrics tied to company-specific impact goals and fund-level impact theses, supporting ongoing performance visibility.

- Linking performance management to impact goals: Accion’s theory of change is aligned with company-level goals against which investment teams’ performance is evaluated annually, and Accion is working to more systematically assess in individual staff performance reviews as well, ensuring consistency between the goals of individual Accion employees and the firm’s strategy.

Practice Example 2.1.

Accion’s Iterative Impact Management and Measurement System

Practice Example 2.2.

Accion’s Impact Framework

Asset Class: Private Equity

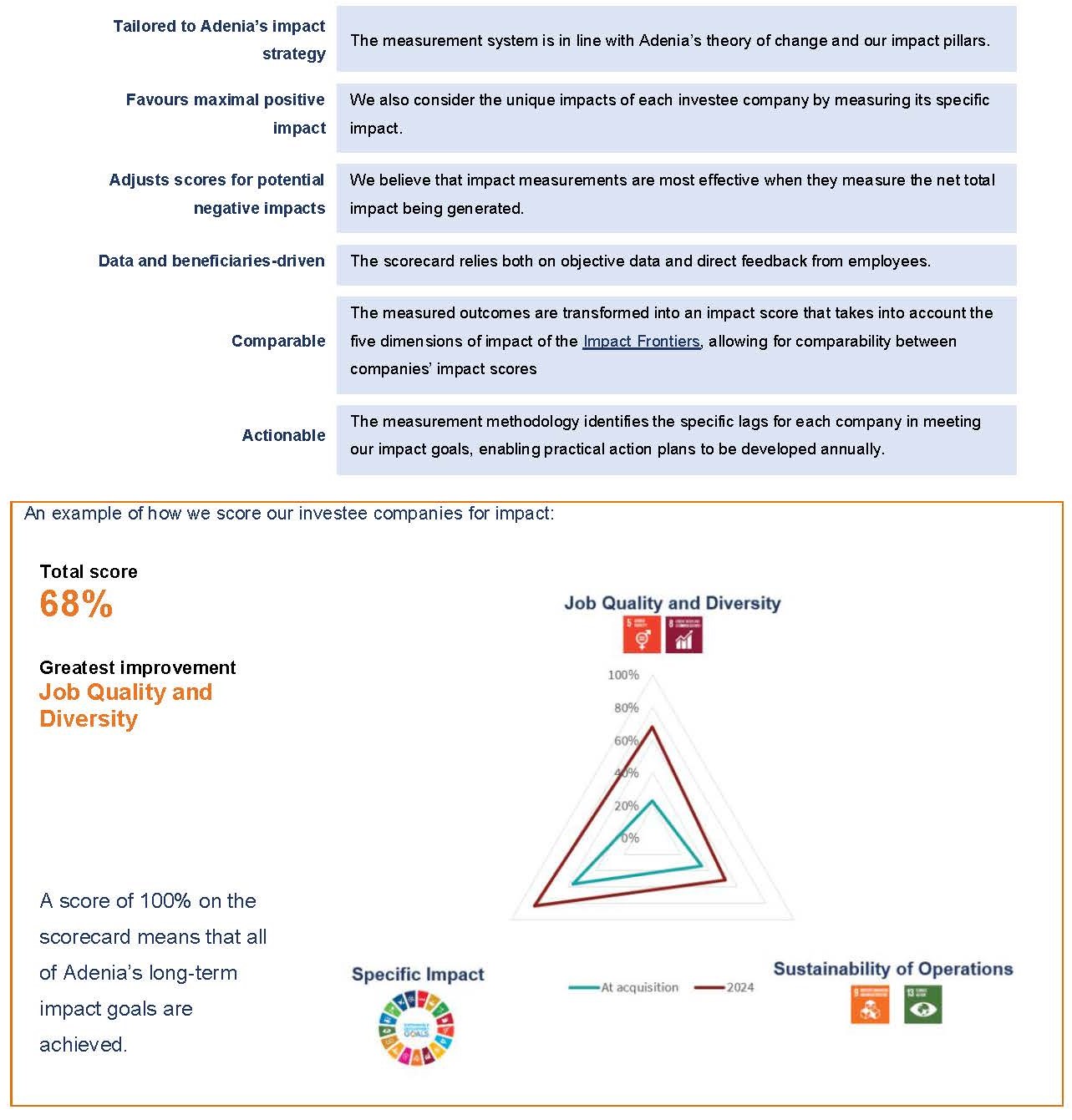

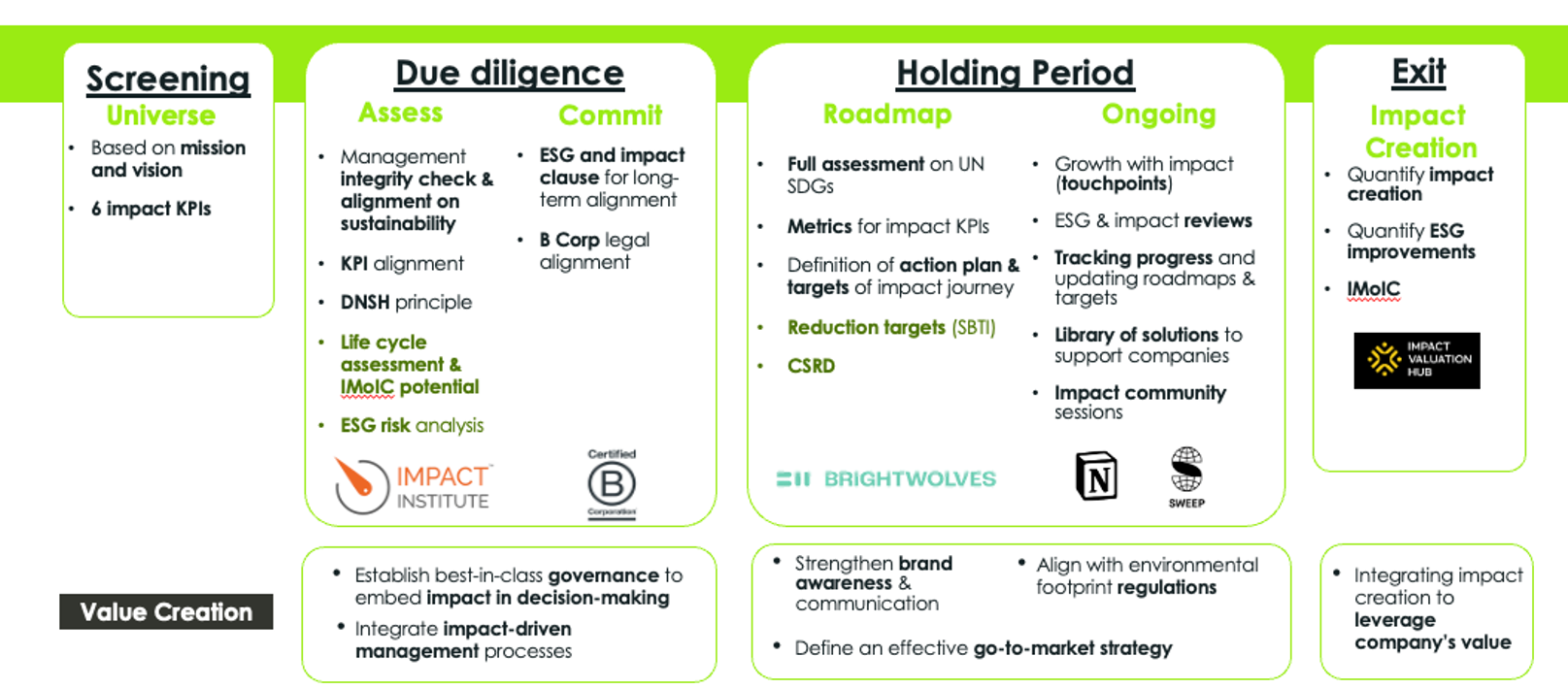

Founded in 2002, Adenia is a private markets investment firm committed to responsible investing for a sustainable Africa. As a control investor, Adenia takes majority ownership positions in its investee companies to create value and drive change with maximum impact. Adenia employs a systematic process to manage impact achievement across its portfolio, using a bespoke impact scorecard to evaluate progress.

- Impact scorecards for evaluating portfolio companies: Adenia uses a proprietary impact scorecard to evaluate impact progress and achievements of its portfolio companies, incorporating both Adenia’s and each investee’s own theory of change. Indicators against which the scorecard tracks impact were developed with reference to the SDGs, IRIS+ and other frameworks. Adenia considers the unique impacts of each investee company in its scorecard by measuring its specific impact and also adjusts scores for potential negative impacts. [See Practice Example 2.3.]

- Portfolio-wide annual score and comparability: The individual investees’ annual scores are aggregated for a portfolio-wide annual score, assessing progress and areas requiring improvement. Adenia uses the Impact Frontiers’ Five Dimensions of Impact, allowing for comparability between companies’ impact scores.

- Built for action: The measurement methodology identifies the specific lags for each company in meeting the impact goals, enabling practical action plans to be developed annually. Leveraging their position as a control investor, each investment manager works closely with respective investee management teams to integrate findings into action plans.

Practice Example 2.3.

Illustrating How Adenia Scores Investee Companies for Impact

Asset Class: Private Equity

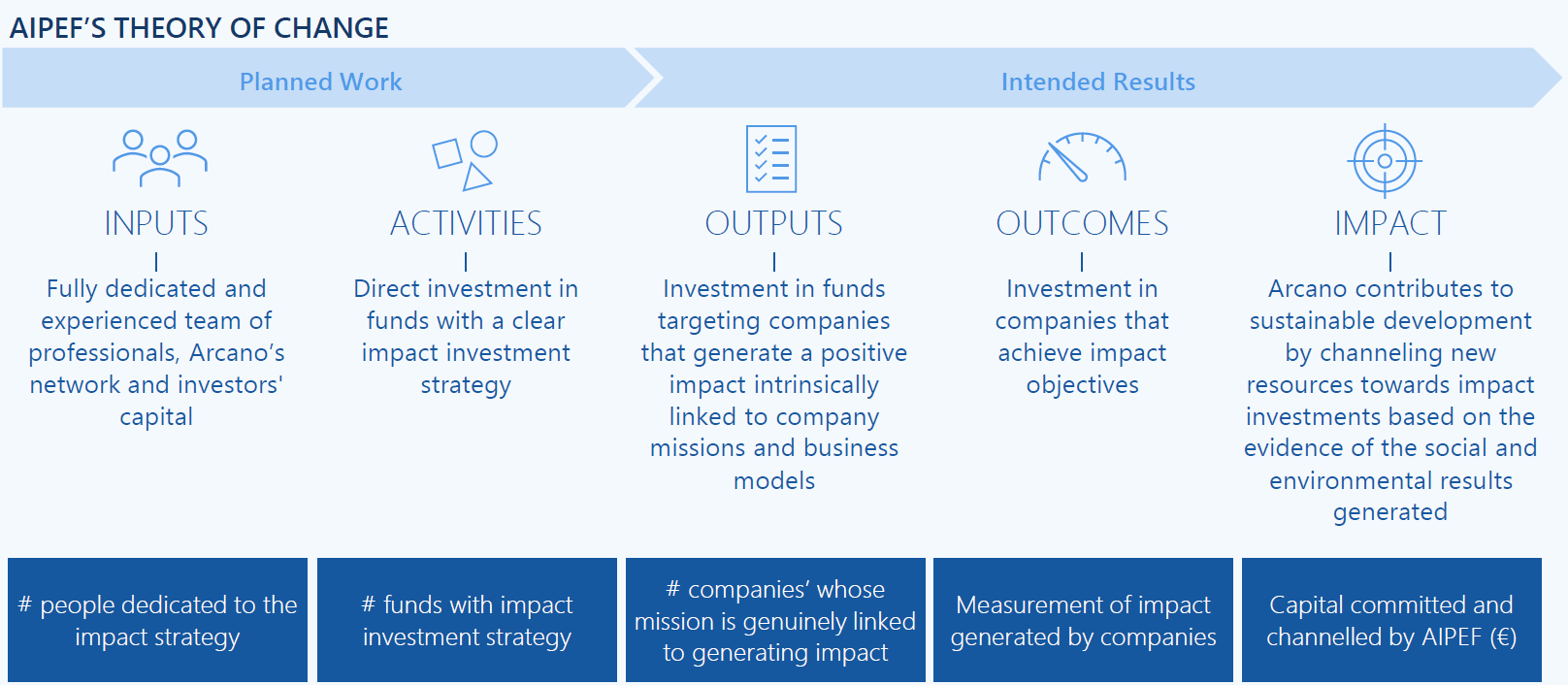

Arcano is a Spanish asset manager investing for impact through a multi-manager approach via its Arcano Impact Private Equity Fund Program (AIPEF). Incorporating a portfolio-level impact measurement and management (IMM) framework, the program targets impact across three core themes: decarbonization, health and wellbeing, and quality education. As a fund-of-funds making indirect investments, Arcano does not engage directly with underlying portfolio companies. Instead, its portfolio-level impact management relies on careful selection, engagement and monitoring of the impact-driven asset managers in which it invests.

- Theory of change-driven strategy and portfolio management: AIPEF has developed a theory of change with clear impact objectives and KPIs for each of its elements. It also systematically monitors the underlying companies’ theories of change to ensure alignment and understand how managers and companies develop their social and environmental goals. [See Practice Example 2.4.]

- Comprehensive due diligence for impact-driven manager selection: Arcano conducts a thorough assessment of prospective managers’ impact intentionality, leveraging its in-house tool: IMPACT Dashboard. Selected managers must be aligned with AIPEF’s impact objectives and demonstrate strong IMM systems, including a commitment to sustaining impact post-exit.

- Setting clear expectations at the time of investment: Arcano includes specific contractual clauses in investment documentation to ensure fund managers implement robust IMM frameworks. Managers are also expected to report impact data in alignment with AIPEF’s impact objectives and KPIs.

- Annual monitoring, ongoing engagement, and continuous improvement: Arcano collects and consolidates impact performance data from its managers on an annual basis. It maintains regular engagement with managers to strengthen its IMM practices and provides technical support where needed. Arcano reports annually on both underlying company and fund level impact data and captures insights from portfolio monitoring in an annual impact report. This report informs strategic decisions and improvements to Arcano’s IMM framework.

Practice Example 2.4.

Arcano’s AIPEF Theory of Change

Asset Class: Venture Capital and Growth Equity

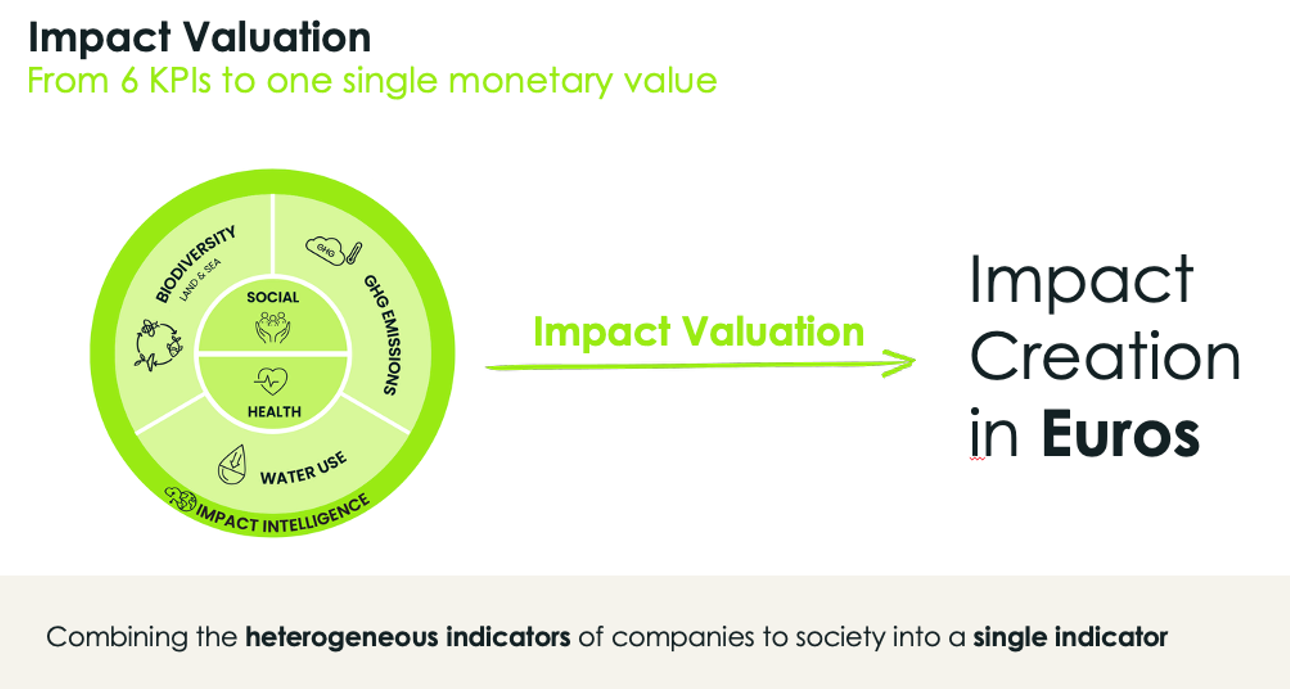

Astanor is an agrifood impact investor with the goal of fostering a global agrifood system that provides nutritious and affordable food for all, preserves and regenerates natural resources, and contributes to decarbonization and the preservation of biodiversity. Central to Astanor’s impact framework and portfolio-wide approach is its proprietary impact valuation model, which converts a variety of impact indicators into a single comparable indicator expressed as a monetary value. [See Practice Examples 2.5 and 2.6.]

- Integration of impact at each step of the investment journey: Starting from initial screening, the investment and impact team collaborate closely with portfolio companies to develop a tailored engagement roadmap. Astanor’s commitment extends beyond the initial stages, as the firm actively works on building and refining ESG and impact measurement practices throughout the entire investment period. This strategic emphasis ensures that sustainability becomes ingrained in the core operations of the company.

- Impact KPIs and impact valuation: With a wide scope of intended impact across its portfolio, Astanor has identified six impact key performance indicators (KPIs), against which it assesses impact potential and measures the performance of individual investments. To promote cross-portfolio consistency and allow comparison, Astanor has developed a proprietary model for impact valuation that converts these heterogeneous indicators into a single monetary value.

- Impact Multiple on Invested Capital (IMoIC): Astanor operationalizes its impact valuation by calculating an IMoIC for each investment, which relates the total monetized impact with the amount of capital invested by the firm. This figure allows the firm to understand its impact performance across its portfolio. By aggregating its portfolio company-level IMoICs, Astanor calculates a fund-level IMoIC that measures its impact creation.

Practice Example 2.5.

Astanor’s Integration of Impact at Each Step of the Investment Journey

Practice Example 2.6.

Astanor’s Impact KPIs and Impact Valuation Approach

Asset Class: Private Equity

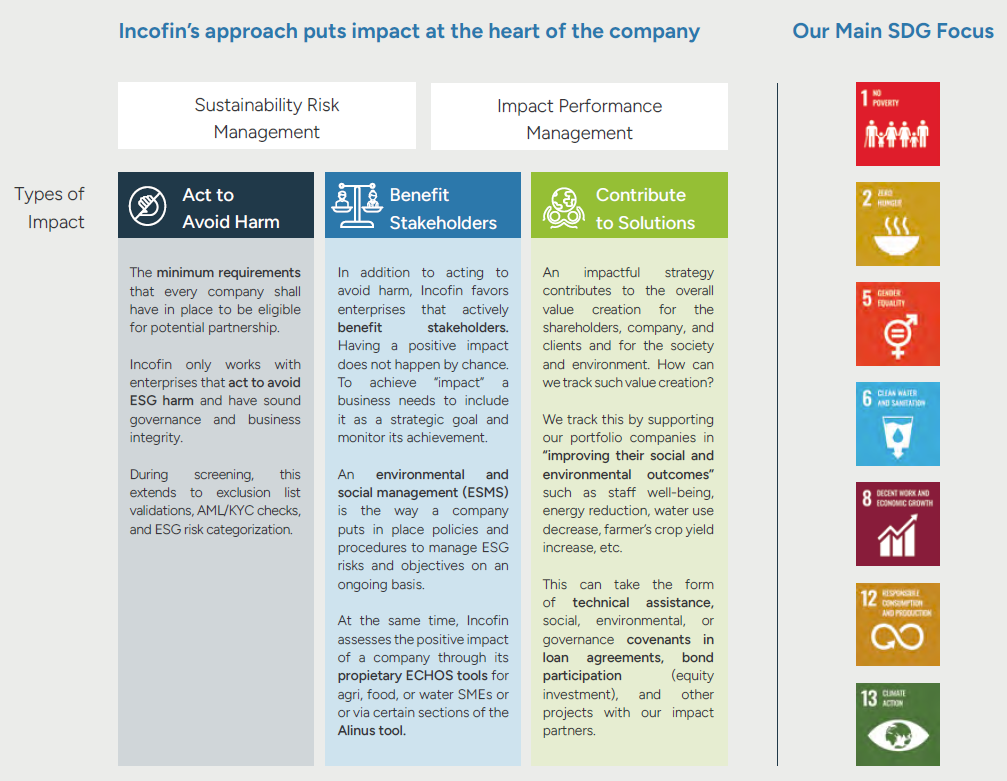

Incofin Investment Management (Incofin IM) invests for impact to drive inclusive progress and sustainable transitions in emerging markets, specializing in inclusive finance, sustainable food and clean water. With over 80 employees across three regional offices and one head office, Incofin IM relies on a clear structure for impact governance. All staff members have a role in impact management, and the firm’s impact framework clarifies responsibilities and ensures accountability for impact management across the investment life cycle. [See Practice Example 2.7.]

- Impact governance with three lines of defense: Incofin IM integrates impact management for both sustainability risks and positive impact at three levels:

- First line of defense: The investment team is responsible for sustainability and impact screening and due diligence, ensuring an integration of financial and impact priorities, as well as ongoing monitoring. Incofin IM provides onboarding training for each new employee and regular refresher on impact assessment.

- Second line of defense: The Risk and ESG team supports the development of frameworks, tools, and processes for sustainability and impact, as well as conducting quality checks, reviewing risky deals, and providing trainings to promote the diffusion of impact across staff operations.

- Third line of defense: the Risk Management Committee and Management Board provide oversight on sustainability risk policy implementation.

- Incentives aligned with annual impact goals: On an annual basis, Incofin’s management board and leadership team develop an impact plan with clear impact goals at the company level. These goals are then translated into individual impact goals for each employee, forming part of their annual performance evaluation and linked to their compensation.

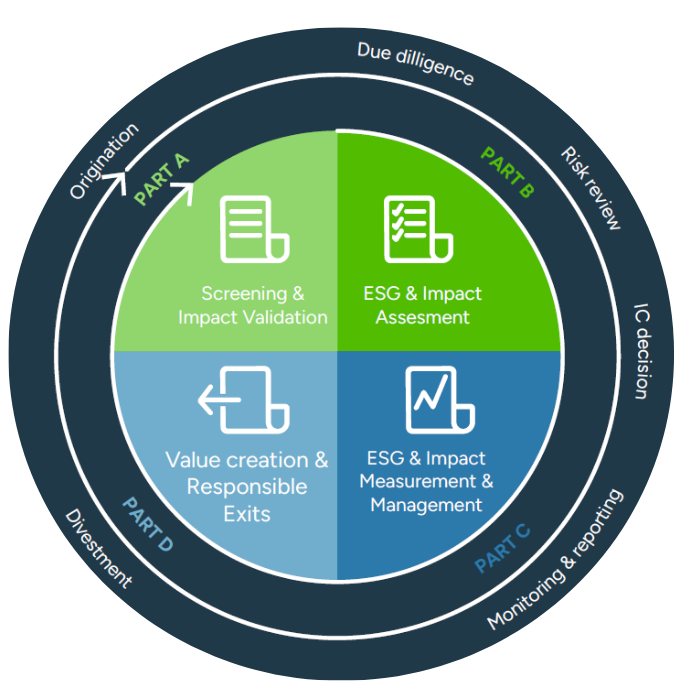

- Impact framework and methodology: Incofin IM uses the ABC impact framework, which recognizes impact as a continuum, from “do no harm” to a more ambitious target of “doing good.” [See Practice Example 2.7.] This is done through a four-step impact methodology across the investment process: screening; due diligence; measuring, managing and reporting; and exit. [See Practice Example 2.8.]

Practice Example 2.7.

The ABC Impact Framework Utilized by Incofin

Practice Example 2.8.

The Four-part Impact Methodology at Incofin IM

Asset Class: Venture Capital

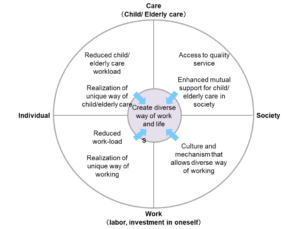

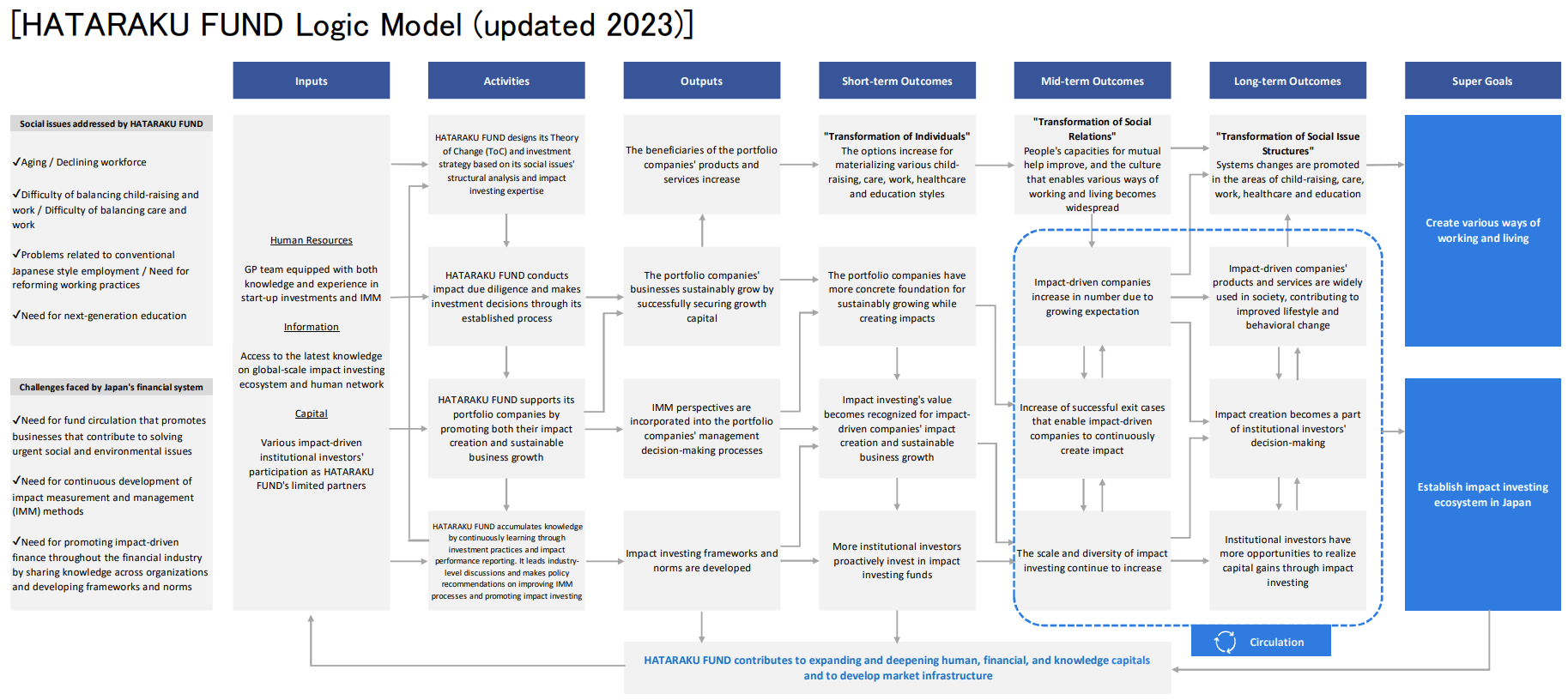

Japan Social Innovation and Investment Foundation (SIIF) is a co-general partner for both the HATARAKU Fund and the SIIFIC Wellness Fund. Established in June 2019, the HATARAKU Fund was one of Japan’s earliest impact funds. Co-managed by Shinsei Impact Investment Limited and SIIF, the Fund entered a market with few domestic precedents for venture-stage impact investing. In response, the fund built a full-cycle IMM approach, adapting global frameworks to suit the Japanese market. SIIF embeds impact from investment selection through post-investment support and exits, with systems to monitor progress at both the deal and portfolio levels.

- Localizing IMM across the investment life cycle: The Fund built its IMM system by referencing global frameworks — such as those from the GIIN, Impact Management Platform and Impact Frontiers — and tailoring them to local needs. These tools are applied throughout the investment life cycle, from due diligence to exit.

- Custom scoring for impact comparability: The Fund developed its own scoring framework that incorporates the Five Dimensions of Impact, plus two additional factors: alignment with the fund’s theory of change and potential for systems change. [See Practice Example 2.9.] Each investment is scored during diligence and reassessed annually, enabling portfolio-level comparability over time. The framework also incorporates the Investor Contribution 2.0 model from Impact Frontiers.

- Institutionalizing practice through tools and documentation: SIIF created detailed manuals for sourcing, due diligence, IMM and exit to formalize its approach and support continuous learning. A shared post-investment support program and a portfolio-level impact dashboard further reinforce consistency and transparency.

Practice Example 2.9.

HATARAKU Fund’s Target Areas Based on Theory of Change and its Logic Model

The Fund’s Logic Model

Footnotes

1 The GIIN’s COMPASS methodology, IRIS+ and the impact performance benchmarks by the Impact Lab are examples of key market-level standardized tools and resources for assessing, analyzing and comparing impact performance.

2 Impact Frontiers’ Impact-Financial Integration norm offers guidance on methods of integrating impact and financial data and analysis. The GIIN’s report on impact lens portfolio construction provides practical guidance for institutional asset owners to apply a holistic portfolio construction approach that balances impact and financial returns.

3 See more on Principle 1 Common and Emerging Practices, Key Observations in the Implementation of Principle 1, “8. LPs aligning impact with managers”.

4 The Impact Linked Compensation report by The ImPact provides comprehensive overview of key considerations and design options and frameworks on the topic.