Introduction

The Common and Emerging Practices, a new series of resources from the Impact Principles, aims to capture key insights from notable trends in common practices in implementing the Impact Principles by our Signatories and highlight promising emerging practices and key gaps. By sharing these common and emerging best practices in impact management, we seek to elevate impact practice in the market and ensure that capital is mobilized at scale with integrity to drive meaningful impact outcomes.

The resources related to Common and Emerging Practices will be released in phases through website publication of initial drafts for each of the nine principles in series, followed by draft and final consolidated reports with stakeholder engagement.

Principle 3

Establish the Manager’s contribution to the achievement of impact

The Manager shall seek to establish and document a credible narrative on its contribution to the achievement of impact for each investment. Contributions can be made through one or more financial and/or non-financial channels. The narrative should be stated in clear terms and supported, as much as possible, by evidence.

The Components of Principle 3

- Establish and document a credible investor contribution to achievement of impact for each investment.

- Contribution can be made through financial or non-financial channels.

- State the narrative in clear terms, supported by evidence.

Overview

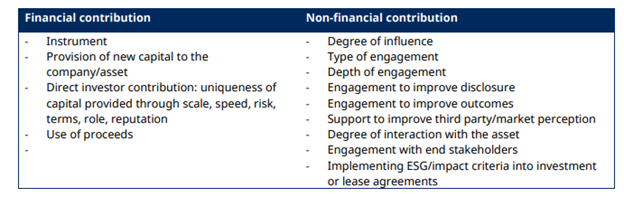

Principle 3 calls on investors to establish their contributions to the achievement of impact for each investment. This contribution — which may be financial or non-financial in nature such as improving the cost of capital, specific financial structuring or active shareholder engagement (see Exhibit 3b) — should be clearly articulated with a credible narrative and supported by evidence as much as possible.

While most Signatories provide a contribution narrative in their disclosures, the depth and specificity of implementation varies widely. Leading Signatories are moving toward more systematic frameworks that embed contribution throughout the investment lifecycle — from strategy and ex-ante assessment to ex-post monitoring or evaluation — in alignment with their theories of change and broader impact management frameworks. A robust implementation of Principle 3 goes beyond generic claims of value-adds and prioritizes specific, evidenced practices with intentionality and supportive capacity.

A Signatory’s position in the impact capital chain,1 along with its investor type, can shape both the focus and nature of its contribution. For many asset owners, financial contributions may be of greater emphasis. Asset managers, especially in venture capital or private equity, may have more non-financial contributions with hands-on engagements with individual portfolio companies.

Challenges in the Implementation of Principle 3

While all Signatories acknowledge and provide narratives to describe their financial and non-financial investor contributions to the achievement of impact, their specificity and level of rigor in implementation practices vary significantly. Key challenges include:

- Vague or generic contribution narratives. Some Signatories describe broad, aspirational contribution intentions without articulating specific actions or levers that contribute to investment outputs or outcomes, through a mechanism like a theory of change, that can be implemented across a portfolio. This may lead to contribution being an ad hoc criteria or afterthought rather than an integral part of investment selection, structuring and engagement strategies. Investors’ level of specificity in their theory of change may also inform the capacity and resourcing needed for execution of their contribution strategies.2

- Monitoring, evidence and feedback loops for contribution effectiveness. While contribution narratives and upfront contribution assessments are common, fewer investors monitor contribution activities and collect direct evidence or stakeholder feedback to understand the effectiveness of their contribution and related impact. A formal evaluation of the effectiveness of investor contribution — as distinct from evaluating investee-level effectiveness or overall impact performance — is relatively rare. A lack of structured, systematic processes to monitor and evaluate contribution practices makes it difficult to assess their effectiveness or inform course correction and improvement over time and across a portfolio.

- Understanding the extent of contribution — attribution and additionality. Determining attribution for social and environmental impact is inherently complex and may not always be required. Many investors find it challenging to delineate their specific role in achieving impact, particularly when multiple actors contribute to outcomes.3 These may include other investors as well as actors and forces in the broader market system and policy environment, with contributions that are often interdependent. Investors’ contribution can also be conflated with investees’ own results, which may or may not have happened without the investors’ involvement, as well as with other market dynamics and external factors. To the extent that it is helpful for investors to understand if their contribution has been additional, there is limited adoption of tools or robust methodologies to distinguish individual investors’ influence from that of others or explicitly link investor contribution to observed outcomes. Some investors — particularly many development financial institutions (DFIs) — prioritize the concept of additionality, which posits that certain impacts would not have occurred without the investor’s involvement, based on the type of capital provided or the profile of the investee or the market. However, it can be difficult to back up claims of additionality with robust ex ante counterfactual analysis, clear evidence and ex post evaluation to demonstrate that an investor’s participation uniquely enabled the impact outcomes, and requiring it in some instances, may leave impact opportunities on the table.4

Key Observations in the Implementation of Principle 3

As implementation of Principle 3 continues to evolve, Signatory disclosures reveal growing efforts to move beyond high-level contribution narratives toward more intentional, structured approaches. Many investors are developing contribution frameworks and tailoring their contribution strategies to reflect their investor type, asset class and role in the impact capital chain. These practices demonstrate increasing integration of investor contribution considerations across the investment lifecycle, although opportunities remain to strengthen ex-post monitoring and review. The following observations highlight how Signatories are advancing contribution practices in their distinct investor contexts and the range of financial and non-financial levers they deploy to enhance impact.

Notable observations include:

1. Development of systematic contribution frameworks. A growing number of Signatories are building dedicated contribution frameworks or embedding it as part of broader impact frameworks, often driven by their theory of change5 and drawing on the Impact Frontier’s Five Dimensions of Impact6. This typically involves identifying intended contribution type and assessing contribution potential ex-ante as part of investment screening and due diligence processes, including by rating or scoring contribution potential. Some Signatories are also establishing processes for monitoring and evaluating contribution activities post investment – such as portfolio surveys and third-party evaluation – creating feedback loops to assess and improve their contribution effectiveness. A systematic contribution framework helps to operationalize an investor’s theory of change, connecting intended inputs and activities for each investment to desired outputs and outcomes.

2. Embedding contribution across the investment lifecycle and the nine principles. Close examination of Signatories’ implementation of Principle 3 demonstrates how investor contribution considerations can be integrated into each stage of the investment lifecycle to strengthen the feedback loop [See Exhibit 3a]. Many Signatories describe how they assess their expected contribution prior to investment — for instance, by using frameworks to evaluate financial or non-financial contribution needs and potential. However, it is less common for investors to explicitly articulate how they monitor, evaluate and refine their contribution strategies over time.7

Exhibit 3a. Embedding Investor Contribution Considerations Across the Investment Lifecycle and the Nine Principles

Exhibit 3b. Examples of Investor Contribution Actions — Financial and Non-Financial

Exhibit 3c. Investor Contribution at Different Levels

- Public sector or development-led investors, such as development finance institutions and multilateral development banks, leverage capital to stimulate broader economic or market-level change with development impact. They deploy both market-rate and concessionary capital or catalytic capital, particularly in emerging and frontier markets. Their contributions often include anchoring first-time or emerging funds, offering de-risking instruments (e.g., guarantees, subordinated capital, FX hedges), to crowd in private capital, and providing technical assistance.

- Philanthropic or impact-first investors, such as foundations and some high net worth individuals and specialized impact funds, seek to maximize social and environmental impact with flexible financial return goals. They fill gaps with grants, program-related investments and risk or patient capital, often supporting early-stage innovation, underserved markets, ecosystem building and field-level impact standards and practices.

- Private sector investors or finance-first and balanced investors, such as institutional asset owners, family offices and many impact-driven commercial asset managers, pursue optimal financial return with flexible positive impact goals or actively seek both strong impact and competitive returns with colinear strategies. They help scale impact investing by creating or supporting mainstream investment products, expanding access to broader institutional and retail audiences, and offering operational and other non-financial support leveraging their platform.

- Direct versus indirect investors: Direct investors in private markets, such as private equity and venture capital general partners (GPs), often contribute through active ownership, strategic guidance and hands-on operational support to companies. They may influence business models, stakeholder practices and impact measurement systems and provide targeted support for underserved markets or innovative solutions. Indirect investors, such as fund-of-funds and asset owners, (e.g., pension funds, insurance, endowments) investing in managers, typically exert influence through capital allocation or signaling with specific mandates, manager selection and engagement, and field-building. They typically place a greater emphasis on financial contribution, for example through catalytic or anchor capital and on shaping manager practices by setting out their expectations in their investor policy statements. More experienced impact leaders in this role may contribute to strengthening the measurement and management capacity of managers by providing guidance, technical assistance or, in rare cases, budget, to advance alignment on impact practices across a portfolio of managers or advance market-building by supporting emerging managers in underserved markets or with new impact strategies.

- Private versus public markets and asset classes. Investments in private markets such as private equity, venture capital, private debt, real estate and infrastructure allow for deeper engagement, customized structuring and active influence. Investments in public markets such as listed equity and fixed income offer fewer direct levers, with contribution often realized through stewardship, shareholder engagement and the design of instruments such as green or social bonds or issuer engagement. Further, the nature of investments within each asset class – such as deal size, duration, ownership stake and control rights – directly affects how and to what extent an investor can contribute to impact outcomes

[See Exhibit 3d.]

Exhibit 3d. Varying Investor Contribution by Asset Classes

Common, Emerging and Nascent Practices in the Implementation of Principle 3

Note: The findings and observations are primarily based on analysis of the most recently published 166 Signatory disclosure statements at the time of the review in early to mid-2024.

Across Signatory disclosures, all investors disclose having a financial or non-financial investor contribution to achievement of impact, though the degree of specificity and depth of these narratives varies considerably. About half of Signatories have begun to incorporate ex-ante assessments of their contribution potential during investment screening and due diligence. However, far fewer go on to conduct ex-post monitoring or evaluation to assess whether those contributions were implemented and effective in practice, highlighting a notable gap between narrative and robust management with evidence-based learning. Systematic contribution frameworks – including defined strategies, ex-ante assessment tools, contribution action plans tailored to each investment and ex-post monitoring – are still emerging practices. These trends highlight a clear opportunity for the field to move beyond narrative toward more intentional, evidence-based contribution practices that are embedded throughout the investment lifecycle with deliberate feedback loops.

Common Practices

(50 to 100% of disclosures)

- Articulating a contribution narrative. All Signatories disclose their investor contribution narratives, with 48% describing both financial and non-financial contributions.

- Non-financial contribution narrative. 93% of Signatories disclose providing non-financial contributions. The most common approaches include:

- Enhancing impact and sustainability practices. 73% disclose influencing or providing support to strengthen investees’ impact or sustainability practices and systems.

- Technical assistance and training: 70% disclose providing technical assistance, advice, training and education.(See other emerging and nascent Signatory practices of non-financial contribution below)

- Financial contribution narrative. 73% of Signatories indicate providing financial contribution with 49% providing specific examples as part of the narrative. They may include providing catalytic capital, signaling or anchoring investments, providing flexible terms or developing innovative financing mechanisms to channel more capital to underserved markets or mainstream impact investing to mobilize capital at scale.

- Ex-ante assessment of contribution. 51% of Signatories disclose conducting ex-ante assessments of investor contribution potential as part of investment screening and due diligence.

Emerging Practices

(25 to 50% of disclosures)

- Organizational capacity building. 42% disclose providing organizational capacity building support beyond impact or sustainability areas, such as strengthening management systems, hiring talent, providing access to markets, supply chains or impact networks as part of their non-financial contribution.

- Shareholder, issuer and other stakeholder engagement. 40% disclose adopting shareholder engagement approaches such as meeting with management and board, engaging in shareholder resolutions and proxy voting (in case of public equities), or engaging with issuers — in the case of fixed income — and other stakeholders as part of their non-financial contribution.

- Systematic contribution framework and strategy. 39% of Signatories disclose having developed a systematic contribution framework and approach which may include ex-ante rating or scoring of contribution potential, ex-post monitoring of contribution results, and development of a clear contribution strategy or action plan for each investment with a set of specific contribution levers.

- Ex-post contribution monitoring. 33% of Signatories disclose conducting ex-post monitoring of contribution activities and results.

- Market or field-building engagements. 28% disclose participating in or supporting industry and field-building activities to contribute to system-level impact as part of their non-financial contribution.

- Catalytic capital. 25% of Signatories disclose providing catalytic capital to mobilize additional capital as part of their financial contribution, sometimes through blended finance structures.

Nascent Practices

(<25% of disclosures)

- Dedicated resourcing for contribution. 23% of Signatories disclose having a dedicated team or capacity focused on contribution, including expert advisors, TA consultants, or value creation or operational teams, available as a resource to investees.

- Taking a board seat. 21% of Signatories disclose serving on the board of the investee, primarily in the case of private equity or venture capital investors, as part of their non-financial contribution.

- Knowledge sharing network. 20% of Signatories discuss providing access to peer networks, ecosystem partners, industry experts and other knowledge sharing opportunities as part of their non-financial contribution.

- Evaluating contribution effectiveness. 15% of Signatories disclose evaluating the effectiveness of their investor contributions, including through third-party evaluation or surveys of investees.

Principle 3 Signatory Practice Spotlights

-

Asset Class: Multiple

AXA Investment Managers (AXA IM), part of the BNP Paribas Group, is an established player in the global asset management industry. With over 3,000 professionals across 24 offices in 19 countries, we serve a broad and international client base, including institutional, corporate, and retail investors.

Through the AXA Impact Investing Strategy, the firm manages a variety of impact funds making direct and fund investments across private equity, venture capital, private debt, real assets, and project finance. With institutional heft, AXA IM contributes to the impact achieved by helping develop and demonstrate the commercial opportunities in the businesses and funds in which they invest.- Closing the financing gap: As a major asset manager, AXA IM plays an important role in demonstrating the commercial potential of impact-aligned investees, including impact-driven enterprises, businesses based in emerging markets, or targeting significant, underserved societal challenges. These investees often face challenges in raising capital, and AXA IM’s investments can signal viability and thereby help them attract additional institutional and private capital.

- Long-term capital provision and partnerships: AXA IM also aims to be a long-term provider of patient capital, acting in partnership with our investees to deliver sustainable impact. This can include providing follow-on capital through funding rounds, as well as serving as a co-investment resource for General Partners (GPs).

- Active investors: AXA IM also seeks to participate in investor-led governance bodies including boards, LPACS, contributing to the delivery of financial and impact priorities.

- Providing a knowledge network: AXA IM makes non-financial contributions by connecting investees to the knowledge and resources of AXA IM and our networks, strengthening our investees’ ability to deliver on their financial and impact objectives

Asset Class: Multiple

BNP Paribas Asset Management (BNPP AM) is a global asset manager with a multi-asset class impact investing platform spanning public and private markets. Reflecting the diversity of its impact strategies, BNPP AM has developed tailored contribution approaches for each asset class and strategy. Across its impact assets, however, BNPP AM is consistent in its commitment to drive contribution through active engagement, while also supporting the broader impact investing field development by participating in industry initiatives.

[See practice example 3.1].- Contribution through issuer engagement in fixed income: For its Green Bond and Social Bond strategies, at issuance, BNPP AM assesses the issuer’s sustainability credentials, its alignment with BNPP AM’s internal taxonomy, and the product’s proposed project ambition, excluding from investment any issuances that fail to meet the firm’s standards. Post-investment, BNPP AM engages the issuer on output and impact indicators and project allocation, excluding or selling a bond if its issuer does not provide indicators or adequately explain its failure to do so.

- Building impact capacity of private equity fund managers: In its private equity fund-of-funds, Towards Impact fund, BNPP AM provides technical advice to help selected fund managers improve their impact management capabilities, thereby promoting impact best practices and developing the private equity impact market. BNPP AM forms long-term partnerships with fund managers and aims to provide additional capital as a co-investment resource.

- Addressing financing gaps for social businesses: In its Social Business Impact Fund, BNPP AM provides financing to non-profits and social enterprises dedicated to achieving impact. To address financing gaps, the firm offers more favorable terms than typically available on the market, such as lower interest rates or flexible liquidity or profitability requirements. BNPP AM also provides support on strategy, management, and governance, taking a seat on investees’ boards when relevant.

- Impact investing field development: BNPP AM contributes to the development of the global impact market by actively participating in various industry initiatives and working groups — including promoting greater transparency around how mainstream asset managers invest for impact and sharing best practices.

Practice Example 3.1

BNPP Social Business Impact – Contribution

Asset Class: Private Equity

Deetken Impact Sustainable Energy (DISE) invests in clean energy and resource efficiency projects across Central America and the Caribbean. In addition to providing long-term, flexible capital, DISE delivers hands-on technical support to strengthen investee capacity, unlock additional investment and accelerate inclusive climate solutions.

- Blended finance to unlock capital at scale: DISE provides equity and quasi-equity project finance to underserved projects, helping de-risk opportunities with investment readiness services and bridge capital gaps in shallow markets. By anchoring the capital stack, DISE expects to catalyze significant multiples in co-investments from project sponsors, senior lenders and other institutional investors.

- Technical assistance to strengthen impact capacity: DISE wraps its investments with targeted technical assistance, including a technical assistance facility funded by IDB Lab through the Scaling Up Renewable Energy Program. This facility supports investees in institutionalizing environmental and social management systems (ESMS), co-designing community-based initiatives and building inclusive business models – enhancing both project quality and long-term viability.

- Accelerating climate finance through regional ecosystem building: Through the Caribbean Inclusive Climate Finance Initiative (CICFI), DISE delivered peer-learning cohorts, individualized investment readiness assessments, and tailored advisory to 16 early-stage climate projects. The program emphasized gender-inclusive climate action, E&S risk management and community engagement. Several participants achieved concrete milestones, including regulatory approvals and debt financing commitments.

Asset Class: Multiple

DEG, a wholly-owned subsidiary of KfW, operates two business lines: (i) its Core Business, offering financial and advisory services to private sector businesses in developing markets from its own funds; and (ii) its promotional program ImpactConnect, which is part of the “Partners in Transformation” offer of the Federal Ministry for Economic Cooperation and Development (BMZ) and provides small-ticket financing of EUR 0.75M–5M on attractive terms. [See practice example 3.2].

(i) Core Business: Alongside long-term finance and risk capital for emerging markets, DEG negotiates transformative actions with its clients and provides advisory services. Through its Development Effectiveness Rating (DERa), which assesses each client’s development contribution, DEG applies a structured, measurable approach to additionality, sharing yearly DERa results with its clients. Considerations include:

-

- Structuring for impact delivery: Contractually agreed transformations during structuring stage based on company assessment — such as stronger governance, or use of funds for gender or green loans — strengthen the company’s position and secure achievement of impact contributions.

- Targeted technical assistance: Through its subsidiary DEG Impulse, DEG offers solutions that help companies to address business challenges and to create developmental impact on social, environmental, or economic issues.

(ii) ImpactConnect: The program supports activities in developing markets that have an impact on development by offering attractive financing to EU-based companies and tracks impact indicators aligned with stakeholder-agreed objectives through its monitoring system.

-

- Technical assistance funding: From ImpactConnect funds, technical assistance grants are provided to enhance portfolio companies’ capacity, structure, or activities with significant developmental or sustainability impact. Leveraging DEG’s network, the ImpactConnect team shares market and sector expertise to support the adoption of recognized sustainable industry practices.

- Monitoring and evaluation of contribution outcomes: To monitor outcomes of investor contribution, ImpactConnect compiles monthly and annual reports, tracking progress against key contribution indicators tied to agreed impact goals. In 2023, an external evaluation was conducted to assess achievement of investor contribution objectives, considering quantitative and qualitative data.

Practice Example 3.2

Promoting Transformation to Drive Client Impact

Asset Class: Multiple (Private Equity, Public Equity and Fixed Income)

Neuberger Berman tailors its investor contribution to the achievement of impact based on the asset class including private equity, public equity and fixed income. The investor tools vary between private and listed markets, but they leverage Neuberger Berman’s strength as an active and long-term owner to advance impact with a multi-asset approach.

- Engagement with private equity partners: NB Private Equity Impact believes that its impact lens can help drive value creation opportunities (i.e., opportunities where the Sponsor can consider factors which can be improved upon in a way that is also accretive to the company value). Specifically, Private Equity Impact does so by guiding managers to better measure impact performance metrics that are aligned with the value proposition of their portfolio companies.

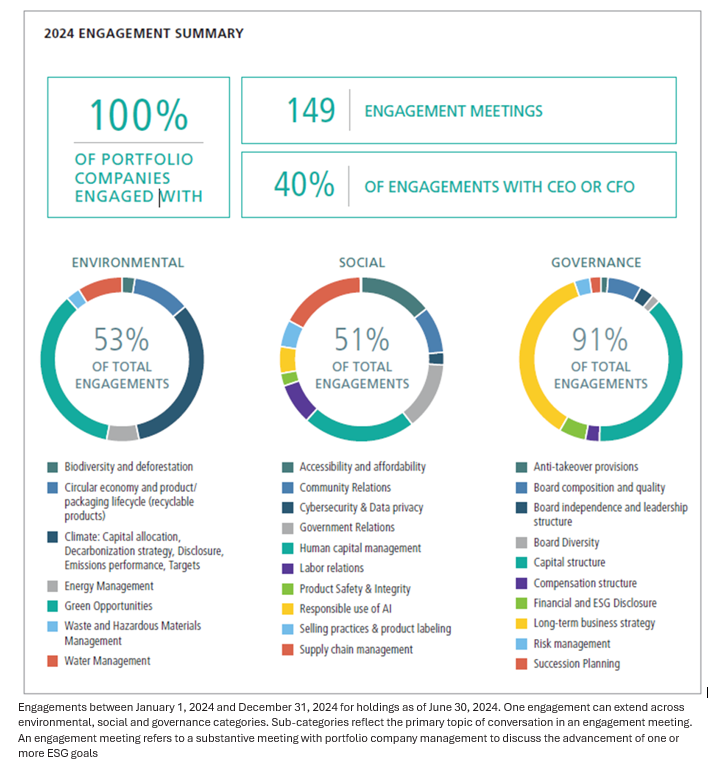

- Active ownership in Public Equity Impact strategies: Engaging with senior management of portfolio companies on capital allocation decisions and outcome target setting is critical to the investor’s impact contribution. Through thoughtful, consistent and long-term oriented engagement, Neuberger Berman can help portfolio companies maximize their impact potential while increasing shareholder value. In 2024, the Equity Impact investment team engaged with 100 percent of portfolio companies through 149 meetings, 40 percent of which included CEOs or CFOs. Annual engagement objectives are set and tracked over time, and new goals are introduced once earlier ones are achieved — supporting a continuous process of investor contribution and active ownership. [See practice example 3.3].

- Contributing to local outcomes through municipal bond selection: The Municipal Impact strategy contributes to community-level impact by directing incremental primary capital to bonds that finance essential infrastructure and public services. These include projects in education, clean water, health and transportation. The strategy targets issuers with a compelling potential for social or environmental impact and applies minimum thresholds for impact evaluation, while prioritizing communities with higher relative needs.

Practice Example 3.3

Neuberger Berman’s Approach to Engagement in Public Equities

Asset Class: Multiple

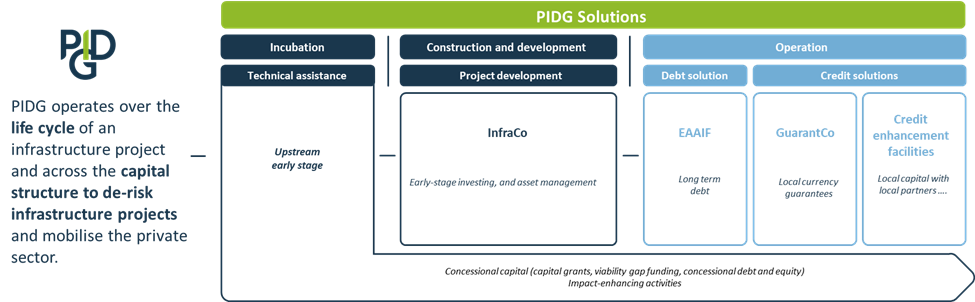

Private Infrastructure Development Group (PIDG) works collaboratively across the project lifecycle and capital structure, deploying grants, equity, long-term debt, and guarantees in hard and local currencies. The investment policy is guided by two core criteria: sustainable development impact and additionality. All investments must support inclusive growth and poverty reduction through improved access to infrastructure. Financing is complemented by knowledge sharing, local capacity building, and efforts to raise standards to make projects both investable and sustainable. Both financial and non-financial contributions are rigorously assessed at appraisal and reviewed throughout the project. By combining catalytic capital and development financing with private finance and expertise, PIDG addresses market failures that impede infrastructure delivery in Africa and Asia.

- Additionality as a prerequisite for engagement: PIDG assesses financial additionality as part of its sustainable impact screening of prospective deals, based on whether private capital is unavailable, insufficient, or not offered on appropriate terms relative to other markets. Engagement must complement, not replace, market actors, typically where real or perceived risks deter private capital. Non-financial additionality is also considered, and where additionality is weak, PIDG will not engage.

- Linking investments to SDG progress: For each investment, PIDG identifies relevant SDG goals and indicators, assesses national progress, and estimates the project’s potential, providing a measure of contribution to the country’s SDG trajectory.

- End-to-end model: PIDG solutions operate across the project lifecycle and capital structure to de-risk projects and mobilize the private sector. [See Practice Example 3.4].

- Incubation phase: PIDG Technical Assistance provides grants and concessional capital — including concessional debt, equity, and viability-gap funding — to enable financial close, with a commercial focus to maximize returns while minimizing market distortions.

- Construction and development phase: The Project Development solution originates, develops, structures, and manages projects from early stage through operation to build a pipeline of bankable opportunities. PIDG also makes equity and other investments in operational businesses and aggregated platforms to enable capital flow and create impact at scale.

- Operation phase: PIDG’s Debt solution, the Emerging Africa & Asia Infrastructure Fund (EAAIF), raises and deploys stable, long-term commercial debt where suitable market financing is lacking to improve project viability, attractiveness and progress towards completion. PIDG’s Guarantee solutions — including GuarantCo and credit-enhancement facilities InfraCredit Nigeria, InfraZamin Pakistan, and Dhamana Guarantee Company in Kenya — help to unlock loans and bonds and mobilize capital for projects and businesses.

Practice Example 3.4

De-risking Infrastructure and Operating across the Project Lifecycle

Asset Class: Fixed Income

RBC Global Asset Management (RBC GAM) manages a suite of impact strategies in the US designed to generate measurable social and environmental outcomes while delivering competitive returns. These strategies are grounded in fixed income investments that direct capital to underserved communities, with a clear focus on capital contribution, allocation, and engagement with loan originators to scale impact. Their main drivers of contribution include:

- Partnering with mission-aligned lenders to expand impact: RBC GAM increases capital availability for underserved communities by partnering with lenders that share similar impact objectives. These include Community Development Financial Institutions (CDFIs), which focus on delivering access to capital in low-income communities. RBC GAM also work with originators such as CDC Small Business Finance to purchase high-quality loans backed by government guarantees, contributing to capital additionality by supporting new lending activity in communities that have historically lacked access.

- Engaging upstream to scale inclusive lending: While direct engagement with loan recipients is often not feasible in fixed income, RBC GAM engages with loan originators to influence lending practices and increase access to credit for underserved borrowers. For example, through a partnership with Groundworks New Mexico and the New Mexico Impact Investment Collaborative, RBC GAM launched LIFT NM, a local impact investing initiative that enables philanthropic investors to channel funds into a liquid fixed income vehicle aligned with community development goals.

- Collaborating to strengthen the market: RBC GAM participates in industry-wide efforts to scale and standardize impact investing, including membership in the Global Impact Investing Network (GIIN) and the Forum for Sustainable and Responsible Investment (US SIF). Through these initiatives, RBC GAM contributes to improving impact data quality and aligning metrics across asset classes.

Asset Class: Multiple

Schroders is a global asset manager with a range of impact-driven strategies across listed equity, listed debt, private equity, real assets, and multi-private asset solutions. Leveraging proprietary tools and an independent impact governance committee, Schroders applies a systematic impact framework across its diverse portfolio, drawing on the expertise of BlueOrchard. Central to its approach is a commitment to investor contribution through both financial and non-financial means, which is systematically assessed through a proprietary impact scorecard and pursued through structured approaches to active ownership and engagement.

- Assessing contribution through a proprietary impact scorecard: Schroders assesses its contribution for each transaction, using a bespoke impact scorecard that draws on Impact Frontiers’ 5 Dimensions of Impact. To isolate the nature of its contribution for each investee, the firm assesses both financial and non-financial contribution across a number of categories. [See Practice Example 3.5].

- Active engagement across asset classes: Schroders emphasizes the need for active engagement that is tightly aligned with impact intent, supports improved impact measurement, and contributes directly to impact outcomes. The firm publishes “Engagement Blueprints” that outline its ambitions, priorities, and expectations for active ownership across public and private markets, identifying and employing the specific levers available to it by asset class. [See Practice Example 3.6].

- Tracking engagement systematically: Schroders tracks the effectiveness of its engagement activities through a proprietary active ownership tool called “Active IQ,” focusing on forward-looking engagement plans and a milestone-based progress tracking system.

Practice Example 3.5

Schroders’ financial and non-financial contribution categories

Practice Example 3.6

Schroders’ approach to listed equity active ownership

Asset Class: Venture Capital

The Hataraku Fund, managed by Shinsei Impact Investment Limited and Japan SIIF, invests in early-stage impact startups promoting diverse ways of working and living in Japan. The Fund assesses its potential investor contribution during due diligence using an impact rating framework based on the Five Dimensions of Impact. Contribution is tracked through both quantitative and qualitative methods and reported annually to limited partners. The Fund considers its contribution to come through two primary channels: business growth support and impact-related support delivered throughout the investment lifecycle.

- Driving business growth through active engagement: Fund members engage with investees at board and shareholder meetings and in monthly strategy sessions to identify challenges and opportunities. They support internal control development, executive recruitment and business planning, while also advising on financing and IPO preparation. By leveraging the networks of Shinsei Impact Investment Limited and the broader SBI Group, the Fund connects investees with potential clients and partners that would otherwise be inaccessible to them.

- Embedding impact strategy from due diligence onward: During due diligence, the Fund co-develops a logic model with each investee to clarify intended outcomes, identify potential risks and project core impact. Post-investment, members support the selection and tracking of evaluation indicators and update the logic model as needed. The Fund also helps investees implement “sustainability management,” which includes articulating mission and social purpose, linking to relevant SDG targets, identifying material sustainability issues and mapping out pathways to impact. These efforts are tailored to each company’s context, often aligned with IPO preparation timelines, and are supported by SBI Group resources where needed.

Asset Class: Infrastructure

STOA is an impact investment fund financing sustainable and resilient infrastructure across Africa, Latin America, and Asia. It supports strategic infrastructure that meets essential needs, such as energy, healthcare, and telecommunication. As an impact fund, STOA makes a unique financial and extra-financial contribution to its infrastructure projects. Its additionality lies in delivering differentiated value and multiplying economic, social, and environmental benefits by promoting high sustainability standards and business integrity.

- Robust investment criteria: Projects are selected based on three pillars: impact, value creation, and risk management. STOA prioritizes high-impact projects evaluated on accessibility (affordable and inclusive services), functionality (reliable and secure delivery), and sustainability (low-carbon footprint), assessed alongside the country’s needs and development potential.

- Proprietary additionality scoring framework: STOA is an additional impact fund, meaning that it makes a unique financial and extra-financial contribution to its infrastructure projects. Additionality means a unique, differentiated contribution. STOA seeks to multiply the benefits of its investments, whether they are economic, social, or environmental. This involves promoting high standards on environmental, social and governance issues (ESG) and in terms of business integrity.

- Targeted non-financial support to build capacity: STOA’s non-financial support to portfolio companies includes access to sustainability expertise via committees, recruitment support, capacity building, and experience sharing. For example, if an investee lacks a sustainability/impact manager, STOA helps recruit a qualified candidate and works to strengthen internal capacities.

Asset Class: Multiple

UBS contributes to the achievement of impact across its wealth and asset management businesses. Its wealth management arm mobilizes client capital into SDG-aligned investment opportunities and supports fund managers and investee companies through strategic engagement and advocacy. The asset management team allocates capital to companies delivering positive social and environmental outcomes and engages directly with portfolio companies to advance the SDGs.

- Evaluating and influencing fund manager impact practices: As an allocator, UBS Global Wealth Management evaluates fund managers not only on financial strength but also on their contribution to impact. Its due diligence and onboarding process includes an assessment of a manager’s additionality, IMM practices and commitment to continuous improvement. UBS regularly engages fund managers on individual deals and portfolio-level approaches and encourages them to become signatories to the Impact Principles to enhance portfolio alignment in impact management.

- Driving SDG alignment through public equity engagement: UBS’s asset management business contributes to impact by allocating capital to listed companies with positive social or environmental outcomes and engaging them on long-term SDG-related objectives. Due diligence includes assessing management’s openness to engagement and the feasibility of achieving progress. Engagement milestones and outcomes are tracked in a central dashboard. While attribution is complex in public markets, UBS uses this process to understand how engagement may contribute to improved impact and financial performance. UBS also collaborated with SDI AOP to develop an outcomes dataset, the first version of which was released in March 2025, to help assess contribution to the SDGs in emerging markets, portfolios’ net-zero goal, or outcomes in specific themes like water or human health. The dataset is also available as a data stream to facilitate consistent reporting and track how investments are contributing to sustainable outcomes over time.

- Building a learning community of managers with engagement practices: UBS’s wealth management business has established a working group with fund managers in its discretionary portfolios focused on measurable outcomes achieved through shareholder and bondholder engagement. This forum enables peer learning and deeper dialogue about driving outcomes through ownership and stewardship practices.

Footnotes

1 The Rockefeller Philanthropy Advisors’ Impact Investing Handbook illustrates the concept of impact capital chain describing a network of stakeholder relationships and the flow of capital between the suppliers of capital (asset owners), users of capital (enterprises) and intermediaries (advisors and asset managers) as well as the ultimate customers and beneficiaries

2 Read more on theory of change and their connection to contribution in the Principle 1 Common and Emerging Practices resource.

3 Impact Frontiers’ Investor Contribution 2.0 project in partnership with The Predistribution Initiative has introduced a Positive Investor Contribution Claim Template as a public resource.

4 While attribution or additionality analysis — with proof points for causality and counterfactual — can be a useful management tool, they are neither core characteristics of impact investing nor requirements under Principle 3. Their application should be guided by the investor’s objectives and contexts, the cost and feasibility of execution, and the potential implications for impact opportunities.

5 Read more on theory of change and their connection to contribution in the Principle 1 Common and Emerging Practices resource.

6 There is variation in how Signatories apply the Five Dimensions of Impact related to contribution dimension. While most Signatories apply it primarily to analyze enterprise or investee-level contribution to outcomes, some Signatories use the framework to evaluate their own investor contribution or both the investor and investees’ contributions.

7 Read more on challenges related to monitoring, evaluating and learning from investor contribution in Challenges section above and in the Principle 8 Common and Emerging Practices.

8 The GIIN’s Guidance for Pursuing Impact in Listed Equities provides further insights on investor contribution approaches in public equity asset class.

9 Tideline, Builders Vision and Bluemark’s report “Scaling Solutions: The Fixed Income Opportunity Hiding in Plain Sight” provides further insights on investor contribution approaches in fixed income asset class.